Market growth steadies in April after first quarter boom

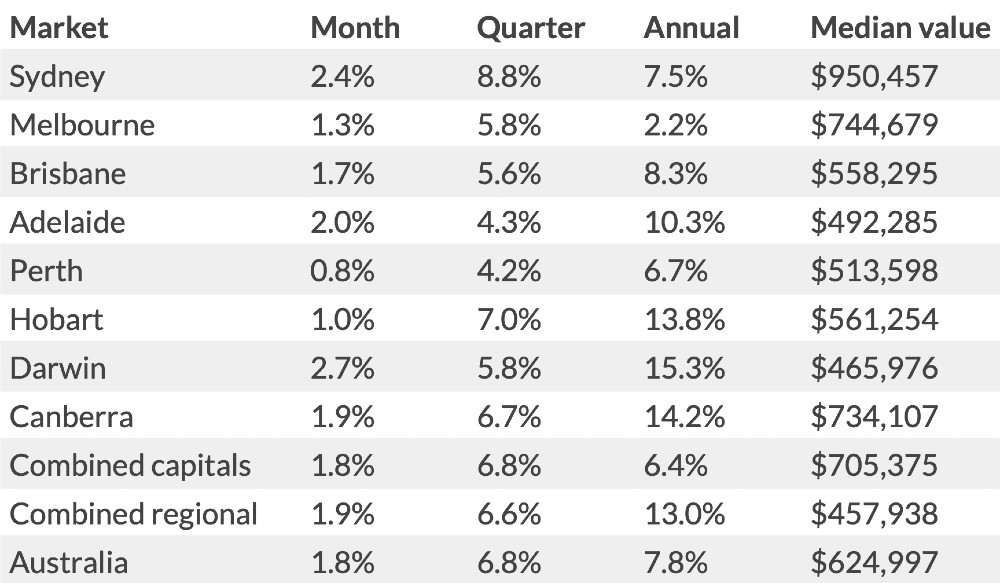

According to CoreLogic’s national home value index, Australian median dwelling prices rose +1.8 per cent in April, an easing from March’s historic growth rate of +2.8 per cent.

The months-long pressure buildup due to increased buyer demand and low stock has been relieved slightly, however conditions remain favourable particularly favourable for sellers.

National property values: April 2021

| Median property value | Monthly change | |

| Houses | $655,557 | +2.0% |

| Units | $553,992 | +1.2% |

The +1.8 per cent increase in property prices around the country bumps the national median dwelling value up to $624,997.

That compounds to a +10.2 per cent total increase from the market’s 2020 low point in September.

CoreLogic’s research director Tim Lawless says the slowdown is "unsurprising given the rapid rate of growth seen over the past six months, especially in the context of subdued wages growth."

"With housing prices rising faster than incomes, it’s likely price sensitive sectors of the market, such as first home buyers and lower income households, are finding it harder to save for a deposit and transactional costs."

The shift is reflected in ABS reports that February and March saw -3.3 and -3.1 per cent drops in the number of first home buyer loans granted—the first time that number has decreased since May 2020—indicating a reduction in the number of people breaking into the market.

While the rate of growth has decreased, it’s still good news on the whole for property owners across the country, with no city or region around Australia recording a drop in median prices.

Darwin and Sydney were the best performing capital cities, clocking +2.7 and +2.4 per cent jumps respectively.

That boost for Sydney brings the city’s median property value ever closer to the $1 million mark, currently sitting on $950,457.

After lagging behind the other capitals in the first quarter of 2021, Adelaide had its strongest month of the year, shooting up +2.0 per cent.

Canberra and Brisbane were also among the better performing cities, growing by +1.9 and +1.7 per cent.

Melbourne was up by +1.3 per cent, and Hobart and Perth saw more significant slowing at +1.0 and +0.8 per cent respectively.

Looking outside of the capitals, regional Tasmania bucked Hobart’s trend by charting a +2.5 per cent increase in property prices for April.

Regional NSW and QLD also turned in stronger than national median numbers with +2.2 per cent and +1.9 per cent gains, while Victoria sat on +1.8 per cent.

The rest of SA didn’t meet Adelaide’s performance, growing just +1.2 per cent, and Regional WA was up just +0.3 per cent.

There’s more new stock being listed, finally

The pressure of low stock on the market has eased as more than 40,000 new properties were listed across the country over the first four weeks of April, nearly +14 per cent above the five year average for the month.

According to Mr Lawless, the rise in new listing numbers signals an improvement in vendor confidence.

"More homeowners are taking advantage of strong selling conditions while they remain skewed towards vendors rather than buyers."

The increase in new stock has had a minimal impact on auction success, though, as the clearance percentage remains in the high 70s. (Clearance rates sat consistently above 80 per cent throughout the first quarter of 2021.)

In fact, April also saw some records broken, with days on market for listed properties down to a median low of 26 days and the median discounting rate down to only 2.7 per cent across the capitals.

This is due to a longer term reduction in total market supply that’s been regularly dropping since 2016 and fell substantially by the end of 2020.

"Total advertised stock levels were -25 per cent below the five year average in late April," Mr Lawless noted.

"Such low total listing numbers, at a time when new listings are above average, reflects the strength of buyer demand, fueling the current rapid rate of absorption.

"Prospective vendors are likely becoming more motivated to test the market thanks to such strong selling conditions as well as housing prices pushing to new record highs in most areas."

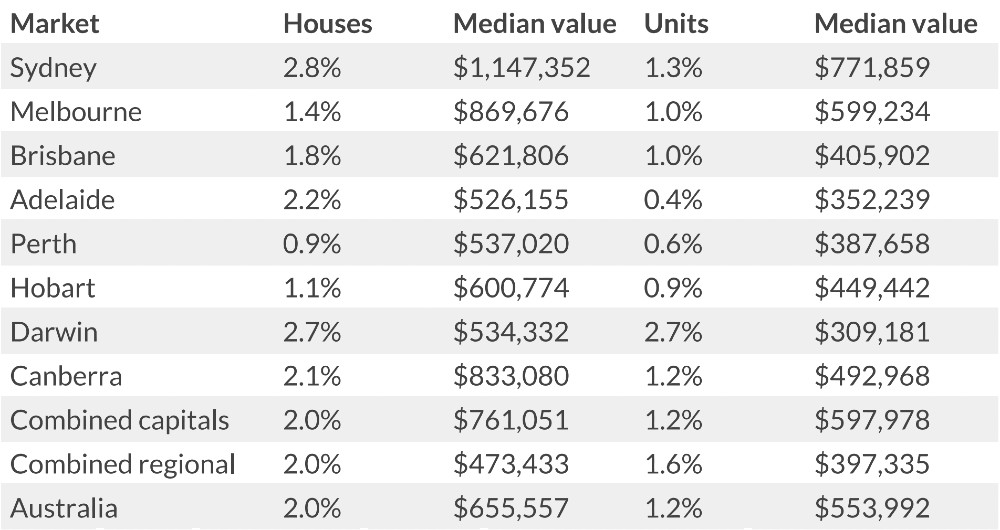

The house and unit markets continue to tell different stories

Nationwide house prices are up a full +2.0 per cent in April compared to a +1.2 per cent bump for units.

The divide continues to be driven by the same combination of factors that have been present since Covid hit, Mr Lawless suggests.

"A preference shift away from higher density housing during a global pandemic is understandable, however a rise in flexible working arrangements also seems to be supporting greater demand for houses around the outer-fringes of capital cities," he said.

"Relatively weak investor activity, compounded by a supply overhang in some high-rise precincts, is also dampening price growth in unit markets."

In Sydney, Brisbane, Adelaide and Canberra, the rate of house price growth was substantially more than for units, though not as vastly different as they were in March.

Those numbers were more in line for Melbourne, Perth and Hobart, with Darwin’s house and unit value increases matching up at +2.7 per cent apiece.

Since the beginning of 2021, capital city house prices have risen +8.6 per cent as opposed to +4.3 per cent for units, and April’s figures seem to indicate that is continuing to grow.

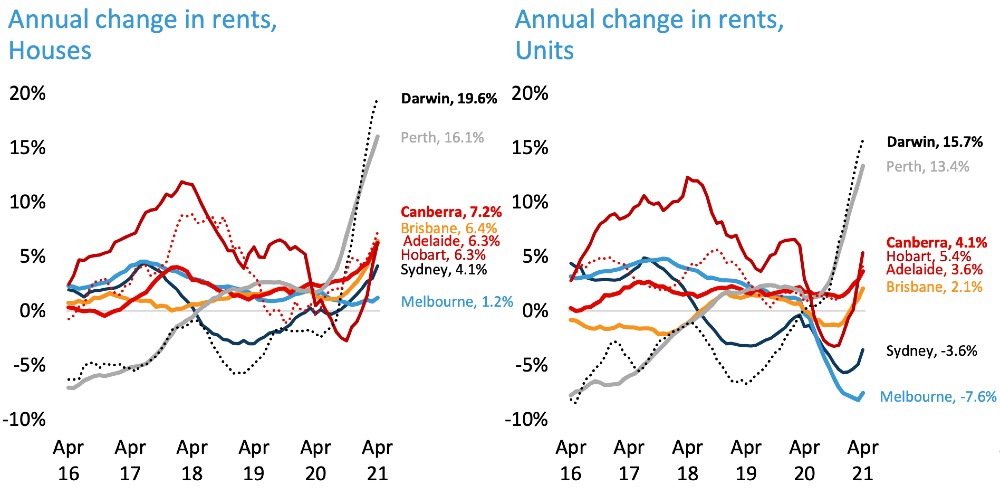

Rents in Sydney and Melbourne stabilise while other capitals thrive

Unlike the relatively broad-based growth being seen in Australian property values this year, the rental market is still behaving quite differently between different cities and states, although April has recorded an uptick in both house and unit rents for all capitals.

Darwin and Perth remain the stars of the country’s rental scene at the moment, with both cities showing double digit percentage rises over the past 12 months.

Renting a house in Darwin costs +17.9 per cent more than it did a year ago, with units close behind on +14.3 per cent.

Despite Perth showing the slowest rate of dwelling value growth in April, its rental market is still soaring skyward, with houses up +14.6 per cent year on year and units up +11.7 per cent.

Meanwhile, rents in Sydney and Melbourne are once again underperforming compared to other cities, units especially.

The key issue driving weaker rental markets in Sydney and Melbourne continues to be Australia’s border closures, as both cities rely heavily on overseas migration.

International students especially make a big impact in high density areas, a stream that has been entirely cut off for the past 12 months.

Canberra, Brisbane, Adelaide and Hobart are all continuing a relatively strong start to 2021, with house rents up between +6.3 and +7.2 per cent and units up between +2.1 and +4.1 per cent year on year.

Investors should be wary that the levels of growth haven’t been enough to catch up with the rate of dwelling prices around the country, as gross rental yields are trending lower.

But CoreLogic notes the majority of markets are showing that landlords are still collecting more in rent than a typical mortgage rate, suggesting that most will be able to keep their investments in the green.

Sydney and Melbourne, are showing the smallest rental return on investment at 2.7 and 2.9 per cent respectively in March, which are record lows for both cities.

"Sydney unit rents have posted a subtle rise over the past three months, while unit rents in Melbourne have held firm over the same period," Mr Lawless explained.

"The improvement comes after a long running decline, however a material improvement in rental conditions is likely to be dependent on foreign students and visitors returning to shore up inner city unit rental demand."

All other capitals are sitting between the 4.3 to 4.5 per cent mark for gross rental yields for March, except for Darwin which has shot through to 6.2 per cent.

Where is the market heading?

Expectations are that median property values will continue to rise throughout 2021, albeit at a less aggressive rate.

CoreLogic’s report concludes that the market has moved through its peak rate of growth, and that the unsustainable boom of the past six months is being slowed by affordability issues, fresh stock on the market, more new detached housing supply and reduced government stimulus.

It’s a prediction that has been echoed by the major banks, who forecast growth to continue through to 2022 but not at the breakneck speeds we’ve seen so far this year.

The combination of sustained low interest rates and strong consumer confidence should keep buyer demand high.

CoreLogic also points out that the RBA and APRA are keeping a close eye on lending standards, and while so far they aren’t noting any serious concerns, any future macroprudential intervention is likely to dampen market activity.