- https://sketchapp.com --%3e %3ctitle%3eIcon/search%3c/title%3e %3cdesc%3eCreated with Sketch.%3c/desc%3e %3cg id='Icon/search' stroke='none' stroke-width='1' fill='none' fill-rule='evenodd' stroke-linecap='round' stroke-linejoin='round'%3e %3ccircle id='Oval' stroke='%23252525' cx='10.5145111' cy='10.5145111' r='6.99455261'%3e%3c/circle%3e %3cpath d='M15.4908752%2c15.4908752 L20.5515137%2c20.5515137' id='Line' stroke='%23252525'%3e%3c/path%3e %3c/g%3e%3c/svg%3e)

Brisbane property market news - key takeaways

- Prices at record highs: The Brisbane property market reached a median dwelling value of $1,126,149 in May 2026, with annual growth of +19.1 per cent placing it among the strongest-performing capitals in the country.

- Listings rising, sales slipping: Total listings climbed +13.6 per cent year on year while sales volumes fell -2.4 per cent, giving buyers noticeably more choice than they had twelve months ago.

- Auctions favour buyers: Brisbane's auction clearance rate sat at just 39.4 per cent in the week ending 14 June 2026, with more than half of all vendors failing to secure a sale under the hammer.

- Rental supply severely constrained: Brisbane's vacancy rate held at 0.9 per cent in May 2026, well below the national rate of 1.2 per cent, with annual rent growth running at +6.6 per cent.

- Rate outlook divided: The RBA cash rate sits at 4.35 per cent, with ANZ, CBA and NAB all forecasting cuts ahead while Westpac predicts two further rises to 4.85 per cent, leaving the borrowing cost outlook genuinely uncertain.

Get a free property value estimate

Find out how much your property is worth in today’s market.

Brisbane property price movements

Brisbane's property market continues to push into record territory, with values rising across every measure in May 2026. The gains are broad-based, covering houses and units alike, though the pace and pattern tell an interesting story beneath the headline numbers.

Brisbane property prices - May 2026

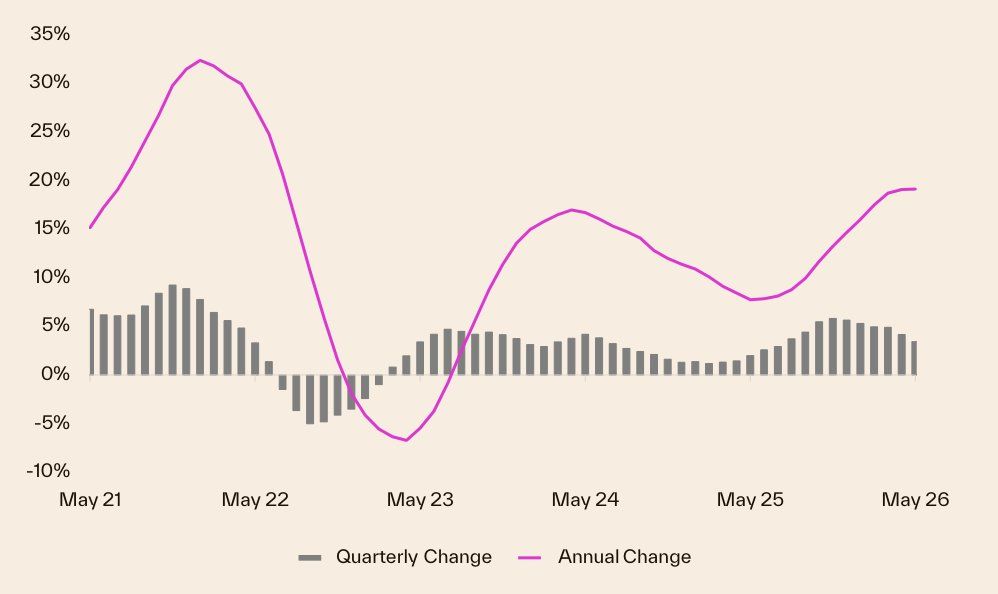

Brisbane homes kept climbing in May 2026, with the combined dwelling value rising +0.9 per cent over the month. The annual gain of +19.1 per cent stands well above the national pace, placing Brisbane among the strongest-performing capital cities in the country.

| Property type | Current median price | Monthly change | Quarterly change | Annual change |

|---|---|---|---|---|

| All Brisbane dwellings | $1,126,149 | +0.9% | +3.4% | +19.1% |

Source: Cotality

The median dwelling value reached $1,126,149 in May 2026, up by around $10,071 from the prior month. Quarterly growth of +3.4 per cent confirms this is not a one-month blip, with Brisbane outpacing a combined capitals market that recorded virtually zero quarterly growth over the same period.

House prices in Brisbane

Brisbane house prices rose +0.8 per cent in May 2026, with the annual gain of +18.6 per cent keeping the Brisbane housing market firmly in growth territory. The quarterly result of +3.3 per cent tells a similar story, with consistent upward momentum sustained across all time horizons.

| Property type | Current median price | Monthly change | Quarterly change | Annual change |

|---|---|---|---|---|

| Brisbane houses | $1,232,690 | +0.8% | +3.3% | +18.6% |

Source: Cotality

The median house value reached $1,232,690, representing a monthly dollar gain of around $9,798. At nearly +19 per cent over the year, house values have added well over $190,000 in twelve months, a pace that continues to reshape affordability for buyers entering the detached market.

Unit prices in Brisbane

Brisbane unit prices outperformed houses in May 2026, rising +1.3 per cent over the month and +21.8 per cent over the year. That annual figure is the sharper of the two, and the gap between unit and house growth rates points to buyers increasingly turning to attached dwellings as house prices push further out of reach.

| Property type | Current median price | Monthly change | Quarterly change | Annual change |

|---|---|---|---|---|

| Brisbane units | $884,881 | +1.3% | +4.1% | +21.8% |

Source: Cotality

The median unit value reached $884,881 in May 2026, up around $11,370 from the prior month. With units gaining +4.1 per cent over the quarter, Brisbane unit prices are running at a faster pace than houses across every time frame measured, a pattern that reflects the growing pull of relative affordability within the city.

Brisbane property market forecasts 2026

Australia's Big Four banks publish annual dwelling price forecasts as part of their economic research, and views on Brisbane for 2026 vary considerably. The spread reflects genuine uncertainty about how the rate environment will play out and how long Brisbane's strong momentum can be sustained.

- CBA predicts Brisbane property prices to rise +12.0 per cent over 2026.

- Westpac predicts Brisbane property prices to rise +9.0 per cent over 2026.

- NAB's published forecast is at the Queensland state level; it predicts dwelling prices to rise +3.8 per cent over the next 12 months across Queensland.

- ANZ predicts Brisbane property prices to rise +9.7 per cent over 2026.

CBA sits as the most bullish on this Brisbane house price forecast, at more than three times NAB's state-level figure of +3.8 per cent. The Brisbane property market predictions from Westpac and ANZ cluster closely together near +9 to +10 per cent, suggesting a reasonable base case sits somewhere in that range, with CBA's +12.0 per cent the clear outlier on the upside. NAB's state-level figure is not directly comparable to the city-level forecasts from the other three banks, so it should be read as a broader Queensland guide rather than a precise Brisbane price trend.

RBA cash rate forecast 2026

The RBA's current cash rate sits at 4.35 per cent, up from the previous rate of 4.10 per cent, with the RBA's own forward guidance pointing to cuts being unlikely until well into 2027. The decision date for the most recent move is not available in current published data. The Big Four banks have divergent views on what happens next.

- ANZ predicts a hold at the RBA's next meeting, with two further cuts in September and December 2027, bringing the cash rate to 3.85 per cent.

- CBA predicts a hold at the RBA's next meeting, with two further cuts in May and September 2027, bringing the cash rate to 3.85 per cent.

- NAB predicts a hold at the RBA's next meeting, with three further cuts in June, September and December 2027, bringing the cash rate to 3.60 per cent.

- Westpac predicts a 25 basis point rise at the RBA's August meeting, with another 25 basis point rise in September, bringing the cash rate to 4.85 per cent.

What this means for the Brisbane market

A cash rate at 4.35 per cent means borrowing costs remain near their cycle highs, compressing what buyers can borrow relative to Brisbane's median dwelling value of $1,126,149. For a city that has recorded +19.1 per cent annual price growth, the gap between what the market is asking and what lenders will approve is a real constraint, particularly for first-home buyers.

The split between the Big Four is unusually wide. ANZ, CBA and NAB all see the next move as a cut, which would ease that borrowing pressure and lend support to the optimistic price forecasts from CBA and ANZ. Westpac's call for two further rises would do the opposite, and if that scenario plays out, forecasts at the upper end of the range would likely need to be revised down.

Units, which are already growing faster than houses in Brisbane at +21.8 per cent annually versus +18.6 per cent for houses, may be more sensitive to rate changes given that buyers in that segment are typically stretching further relative to their incomes.

Several of the Big Four price forecasts were published in Q1 or Q2 2026 and may not yet reflect the full impact of the RBA's most recent rate decision. Bank views on both rates and prices are subject to revision in the months ahead.

Brisbane house prices graphs and charts

Brisbane's house price growth over the last 5 years has been one of the strongest runs of any Australian capital city, and according to Cotality's latest figures, dwelling values rose +0.9 per cent in May 2026, +3.4 per cent over the quarter, and +19.1 per cent over the past year, placing the current dwelling median at $1,126,149.

Brisbane's five-year price story has been shaped by a surge in interstate migration from southern states, a chronic shortfall of new housing supply, and the tailwind of relatively lower prices attracting buyers priced out of Sydney and Melbourne. The cash rate rising to 4.35 per cent put some pressure on borrowing capacity through 2023 and into 2024, yet Brisbane kept climbing, with entry-level and mid-market properties in the city's outer south and south-west corridors absorbing demand that the inner ring could no longer satisfy at scale.

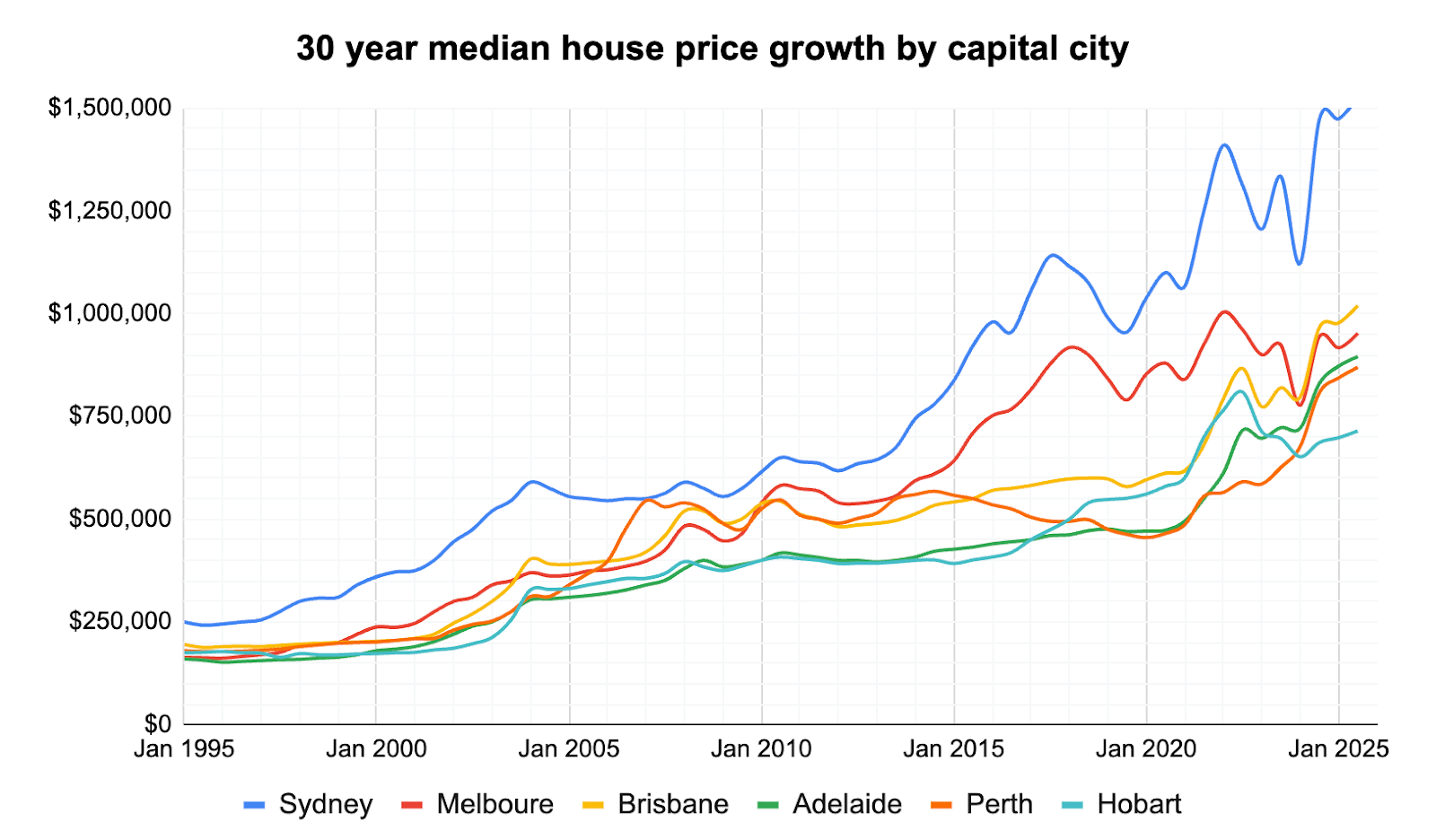

Brisbane property 30 year property price graph

Brisbane property prices growth over the last 10 years has been pronounced, with the city moving from a traditionally affordable capital to one where median house values climbed sharply into the million‑dollar range by late 2025, reflecting years of strong demand and constrained supply. Historical research for Brisbane shows that over the past three decades, low interest rates, sustained population gains and limited new housing have been the main drivers of this long‑run appreciation.

Over the last 30 years, Brisbane has seen repeated cycles of rapid gains and shorter corrections, leaving many homeowners with substantial paper equity while making entry much harder for new buyers. Today, sentiment is mixed: existing owners feel wealthier and are reluctant to sell, while buyers — especially first‑timers — are more cautious because of high prices and elevated mortgage costs; at the same time, tight rental markets and the lead-up to the 2032 Olympics are keeping long‑term confidence relatively strong.

Brisbane selling statistics

Brisbane's selling conditions in May 2026 tell two stories at once. Properties are moving quickly and vendors are conceding less than they were a year ago, yet sales volumes are slipping and listings are building steadily, meaning buyers now have more choice than they did twelve months ago.

Brisbane sales volume and days on market

Brisbane sales volumes fell -2.4 per cent year on year, sitting against a backdrop of combined capitals growth of +1.8 per cent and national growth of +4.1 per cent. At the same time, properties are selling in 20 days on average, down from 21 days a year ago.

| Brisbane sales volume | Brisbane days on market |

|---|---|

| -2.4% Change from 12mo ago | 20 days 21 days 12mo ago |

Source: Cotality

Brisbane's 20-day average is notably faster than the combined capitals figure of 27 days and the national average of 28 days. That gap tells sellers that, despite softer volumes, demand is still translating to quick sales once a buyer is interested, a very different experience from what vendors face in Sydney or Melbourne right now.

Brisbane new and total listings

New listings rose +11.0 per cent year on year, and total listings climbed +13.6 per cent over the same period. Both figures are well ahead of the pace seen twelve months ago.

| Brisbane new listings | Brisbane total listings |

|---|---|

| +11.0% Change from 12mo ago | +13.6% Change from 12mo ago |

Source: Cotality

More stock on the market gives buyers a broader selection and reduces the urgency that drove prices so sharply upward in earlier years. Cameron Kusher, Property Economist, Oz Property Insights, told Oz Property Insights, "Stock for sale in Brisbane, Adelaide, Perth and Darwin remains low but is in a clear upward trend which I expect will continue. Assuming that it does, I would expect this will result in an ongoing slowdown in value growth in these markets too." Rising listings are not a sign of a market in distress, but they do mean sellers can no longer count on scarce supply to do the heavy lifting for them.

Brisbane vendor discount and auction clearance rates

Vendor discount measures the gap between what a seller first asks and what they actually accept. Auction clearance rate measures the share of properties that sell under the hammer on the day. Together, they give a clear read on who holds the stronger hand in negotiations.

Brisbane vendor discount

| May 2026 | May 2025 | |

|---|---|---|

| Brisbane median vendor discount | -2.7% | -3.0% |

Source: Cotality

Brisbane's vendor discount narrowed from -3.0 per cent a year ago to -2.7 per cent in May 2026. Sellers are conceding slightly less ground than they were twelve months ago, which is consistent with the market's fast days-on-market figure and ongoing price growth.

Brisbane auction clearance rates

| Brisbane | 14 Jun 2026 |

|---|---|

| Total Auctions | 142 |

| Sold | 56 |

| Withdrawn | 12 |

| Passed in | 74 |

| Clearance Rate | 39.4% |

Source: Cotality

Brisbane recorded a clearance rate of 39.4 per cent in the week ending 14 June 2026, with 74 of 142 auction results ending in a pass-in. A rate below 50 per cent sits firmly in buyer-favourable territory, well short of the roughly 65-to-70 per cent range that signals a balanced market. At 39.4 per cent, more than half of all vendors who took their property to auction that week did not secure a sale, pointing to a meaningful gap between vendor price expectations and what buyers are currently willing to pay.

Get a deeper insight into how Brisbane sellers are faring in 2026 and what could be on the horizon for the year ahead with some of our latest articles.

Brisbane property investing

Brisbane's rental market remains one of the most active in the country, with rents climbing well above the national pace and vacancy sitting at levels that continue to tilt conditions in favour of landlords. For renters, that means ongoing competition for available properties. For investors, it means strong income growth and relatively low idle risk.

Brisbane rental market

The table below sets out annual rent growth and gross yields for Brisbane and the other capital cities, including a breakdown of house and unit performance where available. It gives a useful read on how Brisbane compares to the national benchmark and where it sits in the yield pecking order.

| Location | Rental rates | Rental yield | Annual change in rents, houses | Annual change in rents, units |

|---|---|---|---|---|

| National | 5.9% | 3.6% | NA | NA |

| Combined Capitals | 5.8% | 3.5% | NA | NA |

| Combined Regional | 5.9% | 4.2% | NA | NA |

| Sydney | 5.8% | 3.2% | 6.3% | 5.1% |

| Melbourne | 4.8% | 3.9% | 4.7% | 4.9% |

| Brisbane | 6.6% | 3.3% | 6.7% | 6.2% |

| Adelaide | 4.5% | 3.4% | 4.5% | 4.6% |

| Perth | 7.5% | 3.6% | 7.4% | 7.8% |

| Hobart | 8.0% | 4.3% | 8.5% | 5.9% |

| Darwin | 10.0% | 6.0% | 10.5% | 9.1% |

| Canberra | 3.3% | 4.1% | 3.9% | 1.9% |

Source: Cotality

Brisbane rents rose +6.6 per cent over the year to May 2026, outpacing both the national rate of +5.9 per cent and every southern capital. House rents led at +6.7 per cent, with units not far behind at +6.2 per cent, showing the pressure is spread across dwelling types rather than concentrated in one segment.

Brisbane's gross yield of 3.3 per cent sits just above Sydney's 3.2 per cent, making it the second-lowest capital after Sydney. That reflects how strongly property values have risen relative to rents: prices have moved fast enough to compress the income return even as rents climb. Investors buying in Brisbane today are accepting a relatively modest yield in exchange for the market's price growth story.

Brisbane vacancy rates

Vacancy rates are the clearest measure of rental tightness. A lower rate means fewer properties are sitting empty, which puts upward pressure on rents. SQM Research data shows Brisbane's vacancy rate held steady at 0.9 per cent in May 2026, unchanged from 0.9 per cent a year earlier.

| Location | May 2026 vacancy rates | May 2026 vacancies | May 2025 vacancy rates | May 2025 vacancies |

|---|---|---|---|---|

| National | 1.2% | 37,844 | 1.2% | 37,879 |

| Sydney | 1.5% | 10,820 | 1.5% | 10,808 |

| Melbourne | 1.6% | 8,446 | 1.7% | 9,074 |

| Brisbane | 0.9% | 3,124 | 0.9% | 3,064 |

| Adelaide | 0.7% | 1,081 | 0.8% | 1,240 |

| Perth | 0.7% | 1,265 | 0.7% | 1,416 |

| Hobart | 0.6% | 161 | 0.6% | 177 |

| Darwin | 0.3% | 75 | 0.5% | 129 |

| Canberra | 1.6% | 970 | 1.5% | 891 |

Source: SQM Research

At 0.9 per cent, Brisbane sits meaningfully below the national rate of 1.2 per cent and well below the 1.5 per cent recorded in Sydney and 1.6 per cent in Melbourne. The number of vacant properties ticked up slightly from 3,064 to 3,124 over the year, but the vacancy rate itself held flat, suggesting population growth absorbed the additional supply without any meaningful easing of conditions.

Louis Christopher, Managing Director at SQM Research said in the latest SQM rental market report:

"The national vacancy rate held steady at 1.2% in May. Where vacancies did rise across a number of cities, that largely reflects normal seasonal patterns — May and June are typically among the higher-vacancy months of the year, outside the December peak, as leasing slows over the cooler months. On a year-on-year basis the market is unchanged, sitting at the same 1.2% as it did in May last year."

For Brisbane, the seasonal softening that Christopher describes has not shifted the dial at all. The city's vacancy rate has been locked at 0.9 per cent for a full year now, meaning even the quieter winter leasing months are not producing any meaningful relief for renters searching for available stock.

That stability at 0.9 per cent, in a period when seasonal patterns would typically nudge vacancies higher, points to a structural supply shortfall rather than a temporary one. For investors, that depth of demand is what continues to drive rent growth at more than twice the national wage growth rate.

Highest growth areas in Brisbane

Brisbane's strongest annual price gains in May 2026 were spread across the city's southern and outer corridors, with the Logan corridor featuring prominently across the top 10. The table below ranks the top 10 Statistical Area Level 3 (SA3) regions for Greater Brisbane by annual percentage change, an SA3 is an Australian Bureau of Statistics geographic unit that typically groups several adjacent suburbs into a single region.

| Rank | SA3 Name | SA4 Name | Median Value | Annual % Change |

|---|---|---|---|---|

| 1 | Beaudesert | Logan - Beaudesert | $953,840 | +24.7% |

| 2 | Loganlea - Carbrook | Logan - Beaudesert | $1,021,565 | +24.1% |

| 3 | Centenary | West | $1,414,515 | +23.8% |

| 4 | Springwood - Kingston | Logan - Beaudesert | $998,510 | +23.5% |

| 5 | Sunnybank | South | $1,406,423 | +23.4% |

| 6 | Beenleigh | Logan - Beaudesert | $925,967 | +23.1% |

| 7 | Strathpine | Moreton Bay - South | $997,820 | +23.0% |

| 8 | Forest Lake - Oxley | Ipswich | $1,009,147 | +22.9% |

| 9 | Nundah | North | $1,194,504 | +22.6% |

| 10 | North Lakes | Moreton Bay - South | $1,063,940 | +22.5% |

Source: Cotality

Highlights for Brisbane's high growth areas

- Beaudesert: Ranked #1 with annual growth of +24.7 per cent and a median value of $953,840, Beaudesert sits at the southern edge of Greater Brisbane where buyers seeking more land and a lower entry price than the inner city continue to push demand. Its position as one of Brisbane's most affordable sub-markets relative to median city values has made it a consistent draw for families and investors alike.

- Loganlea - Carbrook: Ranked #2 with +24.1 per cent annual growth and a median of $1,021,565, this south-Brisbane corridor has benefited from its proximity to major employment nodes along the Logan Motorway and Pacific Motorway. Buyers priced out of closer-in suburbs have increasingly looked to this area as a practical alternative with good transport connections.

- Centenary: Ranked #3 with +23.8 per cent annual growth and a median of $1,414,515, Centenary is the highest-valued SA3 in this top 10 and sits in Brisbane's inner-west. Despite its stronger price point, demand has remained firm, likely supported by its proximity to the CBD and access to established amenity.

- Southern Logan corridor: Ranks #4 through #6, Springwood - Kingston (+23.5 per cent, $998,510), Sunnybank (+23.4 per cent, $1,406,423) and Beenleigh (+23.1 per cent, $925,967), form a broad southern arc where relative affordability and ongoing infrastructure investment in the region have kept buyer interest elevated. Beenleigh's median of $925,967 makes it the most accessibly priced SA3 in the top 10.

- Outer ring: north and west: Ranks #7 through #10, Strathpine (+23.0 per cent, $997,820), Forest Lake - Oxley (+22.9 per cent, $1,009,147), Nundah (+22.6 per cent, $1,194,504) and North Lakes (+22.5 per cent, $1,063,940), span Brisbane's northern and western growth corridors. Strathpine and North Lakes sit within Moreton Bay, where population growth and planned infrastructure upgrades have supported sustained demand, while Nundah offers a more established inner-north option at a relatively higher price point.

View agent & property tools

Our powerful property tools