- https://sketchapp.com --%3e %3ctitle%3eIcon/search%3c/title%3e %3cdesc%3eCreated with Sketch.%3c/desc%3e %3cg id='Icon/search' stroke='none' stroke-width='1' fill='none' fill-rule='evenodd' stroke-linecap='round' stroke-linejoin='round'%3e %3ccircle id='Oval' stroke='%23252525' cx='10.5145111' cy='10.5145111' r='6.99455261'%3e%3c/circle%3e %3cpath d='M15.4908752%2c15.4908752 L20.5515137%2c20.5515137' id='Line' stroke='%23252525'%3e%3c/path%3e %3c/g%3e%3c/svg%3e)

Sydney property market news - key takeaways

- Sydney property market in correction: Sydney dwelling values fell -0.9 per cent in May 2026, the third consecutive monthly decline, leaving prices -2.1 per cent below their November 2025 record high.

- Stock building, buyers gaining ground: Total listings in Sydney rose +9.3 per cent year on year while new listings fell -3.1 per cent, meaning properties are sitting on the market longer and buyers have more choice than at any point in the past year.

- Auctions firmly favour buyers: Sydney's auction clearance rate of 47.2 per cent across 782 auctions for the week ending 14 June 2026 is the lowest result recorded since the Covid lockdown of April 2020, excluding holiday periods.

- Rents rising despite loose vacancy: Sydney rents grew +5.8 per cent over the year to May 2026, with houses (+6.3 per cent) leading units (+5.1 per cent), even as the vacancy rate held steady at 1.5 per cent.

- Rate relief pushed well into 2027: The RBA has lifted the cash rate to 4.35 per cent, and most major banks do not expect meaningful cuts until 2027, keeping borrowing costs elevated for Sydney buyers through the rest of 2026.

Get a free property value estimate

Find out how much your property is worth in today’s market.

Sydney property price movements

Sydney's property market closed May 2026 with values falling for the third consecutive month, continuing a correction that began after the city's record high in November 2025. The declines are broad-based, touching both houses and units, though the two segments are moving at noticeably different speeds.

Sydney property prices — May 2026

Sydney home values eased -0.9 per cent in May 2026, bringing the quarterly change to -2.1 per cent. Annual growth remains positive at +2.3 per cent, though that buffer is shrinking as monthly losses accumulate.

| Property type | Current median price | Monthly change | Quarterly change | Annual change |

|---|---|---|---|---|

| All Sydney dwellings | $1,282,020 | -0.9% | -2.1% | +2.3% |

Source: Cotality

The median Sydney home value of $1,282,020 in May represents a fall of around $11,600 compared to the prior month, based on reversing the monthly movement. Sydney values now sit 2.1 per cent below the record high set in November 2025, meaning the city has given back a meaningful share of the gains made in late 2025.

House prices in Sydney

Sydney house prices fell -1.1 per cent in May 2026, the steepest monthly decline of any dwelling type in the city. The quarterly drop of -2.6 per cent tells a similar story: the Sydney housing market has shifted into clear corrective territory over the past three months.

| Property type | Current median price | Monthly change | Quarterly change | Annual change |

|---|---|---|---|---|

| Sydney houses | $1,579,396 | -1.1% | -2.6% | +2.2% |

Source: Cotality

At a median of $1,579,396, Sydney house values are down roughly $17,600 from the previous month. Tim Lawless, Research Director at Cotality, said in the Cotality Home Value Index that "some cities are now recording falls across the lower quartile, including Sydney and Melbourne's lower quartile houses," suggesting the pressure is not limited to the premium end alone.

Unit prices in Sydney

Sydney unit prices held up better than houses in May 2026, slipping just -0.3 per cent over the month. Sydney unit prices are down -0.9 per cent for the quarter and up +2.4 per cent annually, a more resilient profile than the broader market.

| Property type | Current median price | Monthly change | Quarterly change | Annual change |

|---|---|---|---|---|

| Sydney units | $904,326 | -0.3% | -0.9% | +2.4% |

Source: Cotality

The May median of $904,326 represents a fall of around $2,700 compared to the prior month. Units outperforming houses during a softening period is consistent with a pattern playing out across several capitals, where buyers priced out of the detached house market are gravitating toward more accessible attached dwellings.

Sydney property market forecasts 2026

Australia's Big Four banks publish annual dwelling price forecasts as part of their economic research divisions, and views on Sydney for 2026 vary considerably. Three of the four banks are clustered around modest positive or modest negative outcomes, but one sits well outside that range.

- CBA predicts Sydney property prices to rise +2.0 per cent over 2026.

- Westpac predicts Sydney property prices to fall -3.0 per cent over 2026.

- NAB predicts dwelling prices to rise +1.3 per cent over the next 12 months across New South Wales.

- ANZ predicts Sydney property prices to fall -0.7 per cent over 2026.

The spread between the most and least optimistic Sydney house price forecasts sits at 5.0 percentage points, with CBA at one end and Westpac at the other. ANZ and NAB's New South Wales figure cluster near the middle, suggesting a baseline expectation of minimal movement, positive or negative. The Sydney property market predictions as a whole point to a market where the path is genuinely contested, reflecting how sensitive outcomes will be to the timing and pace of any rate relief.

RBA cash rate forecast 2026

The RBA has raised the cash rate to 4.35 per cent from a previous level of 4.10 per cent, and the broad industry view is that any further cuts are unlikely until well into 2027. The RBA's forward guidance points to persistent inflation as the key reason rate relief remains a 2027 story at the earliest. The four major banks broadly agree the next move is a cut, though they diverge sharply on timing and where rates ultimately settle.

- ANZ predicts a hold at the RBA's next meeting, with two further cuts in September and December 2027, bringing the cash rate to 3.85 per cent.

- CBA predicts a hold at the RBA's next meeting, with two further cuts in May and September 2027, bringing the cash rate to 3.85 per cent.

- NAB predicts a hold at the RBA's next meeting, with three further cuts in June, September and December 2027, bringing the cash rate to 3.60 per cent.

- Westpac predicts a 25 basis point rise at the RBA's August meeting, with another 25 basis point rise in September, bringing the cash rate to 4.85 per cent.

What this means for the Sydney market

A cash rate at 4.35 per cent keeps mortgage repayments elevated at a time when Sydney's median dwelling value sits at $1,282,020. For borrowers in Sydney, the gap between current rates and meaningful relief is wide, and every additional month at this level weighs on purchasing capacity, particularly for first-home buyers and those looking to upgrade.

The divergence between Westpac's outlook and the rest of the pack matters for the Sydney house price forecast. If Westpac is right and rates rise further, the downside scenario for prices becomes considerably sharper than the -3.0 per cent it has already forecast. Even on the more benign scenario from CBA or NAB, rate cuts arriving in 2027 rather than now mean the Sydney market faces a sustained period of pressure through the rest of 2026.

Several of the Big Four forecasts were published earlier in the year, before the most recent RBA decision to raise the cash rate to 4.35 per cent. Some banks may not yet have revised their Sydney or New South Wales outlooks to reflect this change, and updated figures from one or more banks are possible in the months ahead.

Sydney house prices graphs and charts

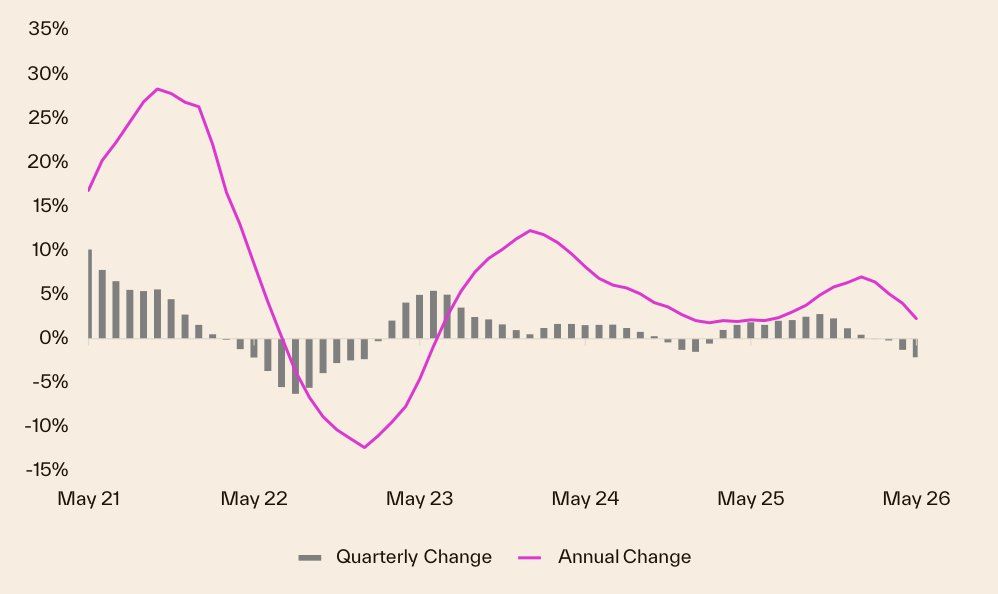

Sydney's house price growth over the last 5 years has carried values to a current dwelling median of $1,282,020, though the most recent data shows the market pulling back, with Cotality's latest figures recording a -0.9 per cent monthly change, a -2.1 per cent quarterly decline, and an annual gain of +2.3 per cent to May 2026.

That five-year arc captured a sharp pandemic-era surge, a rate-driven correction through 2022 and 2023, and a partial recovery before the current slowdown. Rising total listings, a clearance rate that has slipped below 50 per cent, and sustained affordability pressure at Sydney's price levels are all weighing on buyer demand as the market heads into winter 2026.

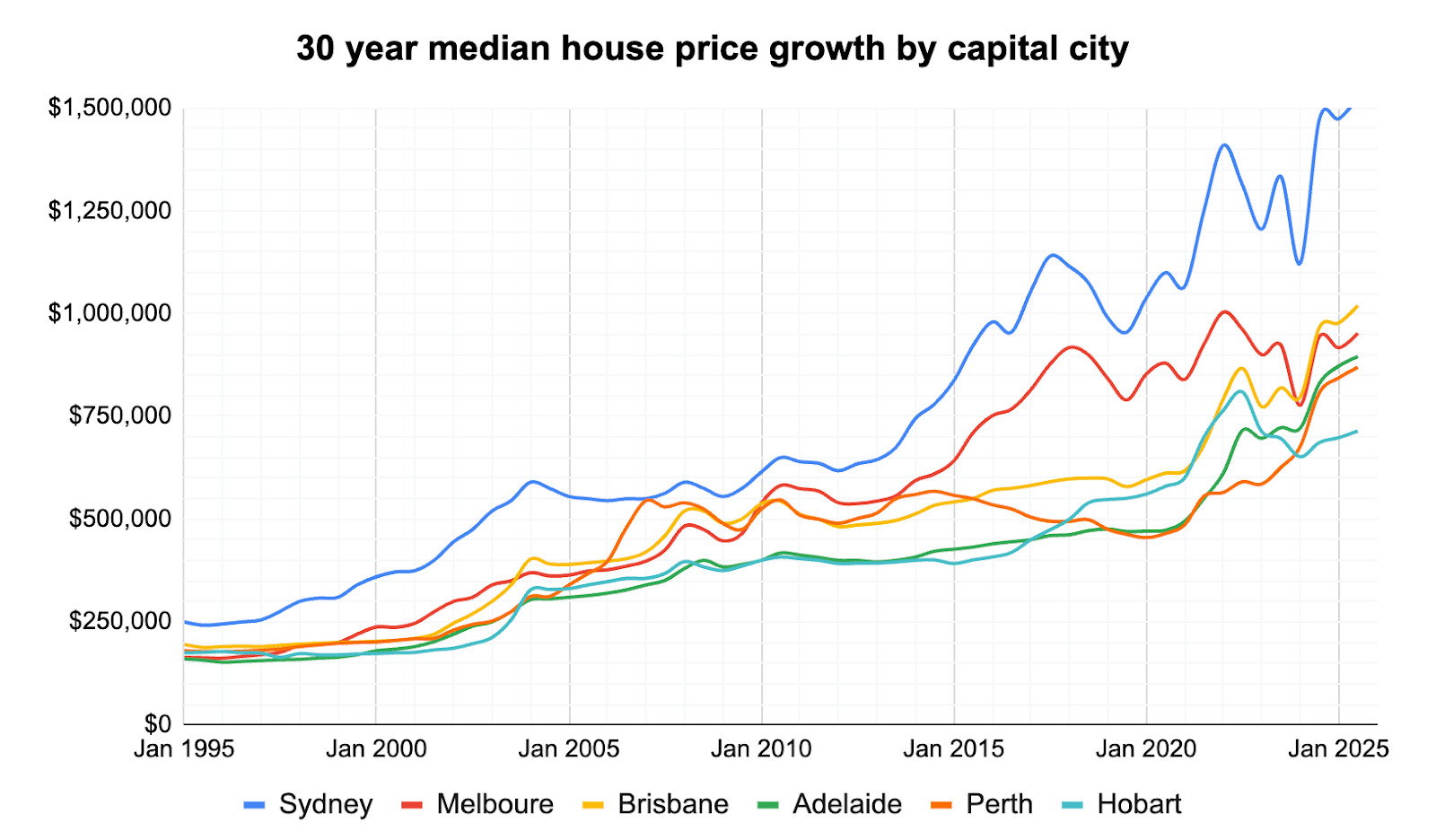

Sydney property 30 year property price graph

Sydney property prices growth over the last 10 years has been strong overall: a large upswing into 2021 was followed by a correction in 2022 and a steady rebuild of momentum through 2023–2025, demonstrating long-run demand, tight supply and the outsized role of interest-rate moves in recent cycles.

Over the past three decades Sydney has recorded some of the biggest cumulative gains in Australia, but the path has been boom–bust–recovery cycles driven by changes in credit, investor activity and population growth; today homeowners feel more cautious than in 2021 while many buyers are still watching rates and affordability, balancing a desire to buy with a need for certainty about repayments and timing.

Sydney selling statistics

The Sydney property market is showing clear signs of a shift in balance between buyers and sellers. Stock is accumulating, auction results are under pressure, and sellers are being asked to work harder to achieve a sale than they were a year ago.

Sydney sales volume and days on market

Sydney sales volume rose just +0.6 per cent year on year in May 2026, well behind the combined capitals average of +1.8 per cent and the national figure of +4.1 per cent. Properties are taking 33 days to sell on average, unchanged from a year ago. That figure sits notably higher than both the combined capitals average of 27 days and the national average of 28 days.

| Sydney sales volume | Sydney days on market |

|---|---|

| 0.6% Change from 12mo ago | 33 days 33 days 12 mo ago |

Source: Cotality

Sydney's days-on-market reading is six days longer than the combined capitals average, a gap that tells buyers they have more time to consider their options than in most other capitals. For sellers, the flat sales volume growth relative to the national pace suggests Sydney's market is absorbing new supply less readily than the broader market.

Sydney new and total listings

New listings in Sydney fell -3.1 per cent year on year, meaning fewer fresh properties are coming to market each month. Total listings, though, rose +9.3 per cent over the same period, according to Cotality's latest figures.

| Sydney new listings | Sydney total listings |

|---|---|

| -3.1% Change from 12mo ago | +9.3% Change from 12mo ago |

Source: Cotality

When new listings fall but total listings rise, it means properties are sitting on the market longer before selling rather than being snapped up quickly. Buyers now have meaningfully more choice than they did a year ago, while sellers face stronger competition from other vendors already in the market.

Sydney vendor discount and auction clearance rates

Vendor discount measures the gap between a property's initial asking price and its final sale price, expressed as a percentage. Auction clearance rates measure the share of properties that sell on auction day. Together, they offer a read on how much negotiating power buyers currently hold and how willing the market is to transact at the prices sellers are asking.

Sydney vendor discount

| May 2026 | May 2025 | |

|---|---|---|

| Sydney median vendor discount | -3.4% | -3.5% |

Source: Cotality

Sydney's vendor discount sits at -3.4 per cent, barely changed from -3.5 per cent a year ago. Sellers are conceding roughly the same slice of their asking price as they were twelve months ago, suggesting that while conditions have softened, most vendors are not yet making dramatic price concessions to secure a sale.

Sydney auction clearance rates

| Sydney | 14 Jun 2026 |

|---|---|

| Total Auctions | 782 |

| Sold | 369 |

| Withdrawn | 167 |

| Passed in | 245 |

| Clearance Rate | 47.2% |

Source: Cotality

Sydney recorded a clearance rate of 47.2 per cent across 782 auctions for the week ending 14 June 2026, a result that sits firmly in buyer-favourable territory. A rate below 50 per cent means more properties passed in or were withdrawn than sold under the hammer. With 245 properties passed in and 167 withdrawn on the same day, a substantial share of vendors did not achieve a sale.

Louis Christopher, Managing Director at SQM Research, said "This week's auction clearance rate for Sydney is the lowest recorded since the Covid lockdown of April 2020 (excluding holiday periods)."

Get a deeper insight into how Sydney sellers are faring in 2026 and what could be on the horizon for the the year ahead with some of our latest articles.

Sydney property investing

Sydney's rental market continues to reward landlords with steady income growth, even as property values soften. For renters, conditions remain tight: vacancy is low and annual rent increases are running well ahead of inflation.

Sydney rental market

The table below covers annual rent change, gross rental yield, and the house and unit rent breakdown for Sydney and all major Australian markets. These figures give both investors and renters a clear picture of how Sydney stacks up nationally.

| Location | Rental rates | Rental yield | Annual change in rents, houses | Annual change in rents, units |

|---|---|---|---|---|

| National | 5.9% | 3.6% | NA | NA |

| Combined Capitals | 5.8% | 3.5% | NA | NA |

| Combined Regional | 5.9% | 4.2% | NA | NA |

| Sydney | 5.8% | 3.2% | 6.3% | 5.1% |

| Melbourne | 4.8% | 3.9% | 4.7% | 4.9% |

| Brisbane | 6.6% | 3.3% | 6.7% | 6.2% |

| Adelaide | 4.5% | 3.4% | 4.5% | 4.6% |

| Perth | 7.5% | 3.6% | 7.4% | 7.8% |

| Hobart | 8.0% | 4.3% | 8.5% | 5.9% |

| Darwin | 10.0% | 6.0% | 10.5% | 9.1% |

| Canberra | 3.3% | 4.1% | 3.9% | 1.9% |

Source: Cotality

Sydney's rents rose +5.8 per cent over the year to May 2026, matching the combined capitals average, with houses (+6.3 per cent) outpacing units (+5.1 per cent). At 3.2 per cent, Sydney's gross yield is the lowest of any capital city, reflecting how far property values have run relative to rental income.

For investors chasing yield, Sydney is the toughest market in the country. That said, strong rent growth does mean the gap between purchase price and rental income is at least narrowing, if slowly.

Sydney vacancy rates

The vacancy rate is the share of rental properties sitting empty at any given time. A lower rate means fewer options for renters and more pricing power for landlords. SQM Research data shows Sydney's vacancy rate held at 1.5 per cent in May 2026, unchanged from 1.5 per cent a year earlier.

| Location | May 2026 vacancy rates | May 2026 vacancies | May 2025 vacancy rates | May 2025 vacancies |

|---|---|---|---|---|

| National | 1.2% | 37,844 | 1.2% | 37,879 |

| Sydney | 1.5% | 10,820 | 1.5% | 10,808 |

| Melbourne | 1.6% | 8,446 | 1.7% | 9,074 |

| Brisbane | 0.9% | 3,124 | 0.9% | 3,064 |

| Adelaide | 0.7% | 1,081 | 0.8% | 1,240 |

| Perth | 0.7% | 1,265 | 0.7% | 1,416 |

| Hobart | 0.6% | 161 | 0.6% | 177 |

| Darwin | 0.3% | 75 | 0.5% | 129 |

| Canberra | 1.6% | 970 | 1.5% | 891 |

Source: SQM Research

Sydney sits above the national rate of 1.2 per cent, making it the most loosely supplied major rental market alongside Melbourne and Canberra. Brisbane, Adelaide, Perth and Hobart are all running well below 1 per cent, pointing to far more acute rental pressure in those cities. Sydney's flat year-on-year reading, at exactly 10,820 vacant properties versus 10,808 a year ago, shows the market has barely moved in either direction.

Louis Christopher, Managing Director at SQM Research said in the latest SQM rental market report:

"The national vacancy rate held steady at 1.2% in May. Where vacancies did rise across a number of cities, that largely reflects normal seasonal patterns — May and June are typically among the higher-vacancy months of the year, outside the December peak, as leasing slows over the cooler months. On a year-on-year basis the market is unchanged, sitting at the same 1.2% as it did in May last year."

For Sydney specifically, the seasonal caution in this observation is worth keeping in mind. The city's vacancy rate has not budged year on year, but a flat reading through the typically slower winter leasing months suggests underlying demand is absorbing supply reasonably well. Louis Christopher, Managing Director at SQM Research told the SQM Research Weekly Newsletter that "Sydney is marginally tighter than it was a year ago," which adds further weight to the view that the headline 1.5 per cent figure may be understating the market's competitiveness for renters.

Highest growth areas in Sydney

Sydney's strongest annual price gains in May 2026 came from the city's outer western, outer south-western and Central Coast corridors. The table below ranks the top 10 Statistical Area Level 3 (SA3) regions across Greater Sydney by annual percentage change, an SA3 is an Australian Bureau of Statistics geographic classification that typically groups several adjacent suburbs into a single region.

| Rank | SA3 Name | SA4 Name | Median Value | Annual % Change |

|---|---|---|---|---|

| 1 | Penrith | Outer West and Blue Mountains | $1,110,032 | +11.7% |

| 2 | St Marys | Outer West and Blue Mountains | $1,139,380 | +11.6% |

| 3 | Wyong | Central Coast | $967,538 | +11.0% |

| 4 | Campbelltown | Outer South West | $1,024,514 | +10.6% |

| 5 | Richmond - Windsor | Outer West and Blue Mountains | $993,312 | +10.6% |

| 6 | Mount Druitt | Blacktown | $1,024,361 | +10.5% |

| 7 | Bringelly - Green Valley | South West | $1,264,331 | +10.4% |

| 8 | Merrylands - Guildford | Parramatta | $1,305,665 | +9.8% |

| 9 | Camden | Outer South West | $1,224,041 | +9.6% |

| 10 | Sutherland - Menai - Heathcote | Sutherland | $1,640,710 | +9.2% |

Source: Cotality

Highlights for Sydney’s high growth areas

- Penrith: Ranked #1 with annual growth of +11.7 per cent and a median value of $1,110,032, Penrith leads Greater Sydney's growth table by a clear margin. Its relative affordability compared to middle-ring suburbs, combined with ongoing infrastructure investment in Sydney's outer west, continues to draw buyers further from the city centre.

- St Marys: Ranked #2 with +11.6 per cent annual growth and a median of $1,139,380, St Marys sits just a fraction behind its Outer West and Blue Mountains neighbour Penrith. The area appeals to buyers seeking established housing stock at a price point still below the Sydney dwelling median of $1,282,020.

- Wyong: Ranked #3 with +11.0 per cent annual growth and a median of $967,538, Wyong is the only region in the top 10 with a median below $1,000,000. Its position on the Central Coast, combined with improved rail access to Sydney, makes it one of the more accessible entry points into the broader Greater Sydney market.

- Outer south-west affordability belt: Ranks #4 through #6, Campbelltown (NSW) (+10.6 per cent, $1,024,514), Richmond - Windsor (+10.6 per cent, $993,312) and Mount Druitt (+10.5 per cent, $1,024,361), form a band of sub-$1,050,000 medians stretching across Sydney's outer south-west and north-west. Buyers priced out of inner and middle-ring markets have been a consistent source of demand across these areas, keeping growth rates well above the city-wide annual average of +2.3 per cent.

- South-west growth corridor and Sutherland outlier: Ranks #7 through #9, Bringelly - Green Valley (+10.4 per cent, $1,264,331), Merrylands - Guildford (+9.8 per cent, $1,305,665) and Camden (+9.6 per cent, $1,224,041), reflect continued demand pressure in Sydney's expanding south-western growth corridor. At rank #10, Sutherland - Menai - Heathcote stands apart from the broader outer-suburb theme, posting +9.2 per cent annual growth on a median of $1,640,710, suggesting that prestige lifestyle suburbs in Sydney's south can still attract strong buyer interest even as the city's overall price momentum softens.

View agent & property tools

Our powerful property tools