- https://sketchapp.com --%3e %3ctitle%3eIcon/search%3c/title%3e %3cdesc%3eCreated with Sketch.%3c/desc%3e %3cg id='Icon/search' stroke='none' stroke-width='1' fill='none' fill-rule='evenodd' stroke-linecap='round' stroke-linejoin='round'%3e %3ccircle id='Oval' stroke='%23252525' cx='10.5145111' cy='10.5145111' r='6.99455261'%3e%3c/circle%3e %3cpath d='M15.4908752%2c15.4908752 L20.5515137%2c20.5515137' id='Line' stroke='%23252525'%3e%3c/path%3e %3c/g%3e%3c/svg%3e)

Melbourne property market news - key takeaways

- Melbourne property market softening: Melbourne dwelling values fell -1.0 per cent in June 2026 and -2.6 per cent over the quarter, with the median now sitting -4.0 per cent below the March 2022 peak.

- Stock rising, homes sitting longer: Total listings climbed +17.4 per cent year on year, and the median days on market extended to 36 days, six days longer than the average capital city home.

- Buyers hold the edge at auction: Melbourne recorded an auction clearance rate of 50.4 per cent for the week ending 12 July 2026, a soft result that places conditions firmly in buyer-favourable territory.

- Rents rising despite easing values: Melbourne rents grew +4.9 per cent annually, with a vacancy rate that has tightened from 1.8 per cent a year ago to 1.6 per cent, supporting a gross rental yield of 3.9 per cent.

- Rate outlook split among lenders: The RBA cash rate sits at 4.35 per cent, with three of the Big Four banks forecasting eventual cuts and Westpac forecasting further rises, leaving the rate path genuinely uncertain for the rest of 2026.

Get a free property value estimate

Find out how much your property is worth in today’s market.

Melbourne property price movements

Melbourne home values fell -1.0 per cent in June 2026, extending a run of monthly declines that has now pushed the quarterly result to -2.6 per cent. On an annual basis, values are -0.9 per cent lower than a year ago.

Melbourne property prices - June 2026

| Property type | Current median price | Monthly change | Quarterly change | Annual change |

|---|---|---|---|---|

| All Melbourne dwellings | $808,486 | -1.0% | -2.6% | -0.9% |

Source: Cotality

The median home value in Melbourne stood at $808,486 in June 2026, down around $8,166 over the month. Values remain -4.0 per cent below their March 2022 peak, meaning the gap to that record high has widened slightly as monthly declines continue to accumulate.

House prices in Melbourne

Melbourne house prices fell -1.3 per cent in June 2026, the steepest monthly decline across all property types in the city. The quarterly result of -3.3 per cent shows the pressure on Melbourne housing market conditions has been consistent rather than concentrated in a single month.

| Property type | Current median price | Monthly change | Quarterly change | Annual change |

|---|---|---|---|---|

| Melbourne houses | $948,482 | -1.3% | -3.3% | -1.2% |

Source: Cotality

The median house value sat at $948,482 in June 2026, a fall of around $12,481 over the month. On an annual basis, house values are -1.2 per cent lower than a year ago, a deeper slide than the broader all-properties figure, suggesting houses have borne more of the correction than units.

Unit prices in Melbourne

Melbourne unit prices eased -0.4 per cent in June 2026, a more modest monthly movement than the house segment. The annual change of -0.2 per cent shows Melbourne unit prices have held relatively close to flat over the past year.

| Property type | Current median price | Monthly change | Quarterly change | Annual change |

|---|---|---|---|---|

| Melbourne units | $637,170 | -0.4% | -1.0% | -0.2% |

Source: Cotality

The median unit value was $637,170 in June 2026, slipping around $2,557 over the month. That monthly dollar change is considerably smaller than the house segment, and with a quarterly decline of -1.0 per cent against houses at -3.3 per cent, units have proved noticeably more resilient through this softer period.

Melbourne property market forecasts 2026

Australia's Big Four banks publish house price forecasts each year as part of their economic research programmes, and their views on Melbourne for 2026 cover a wide range. All four have published city-level or state-level figures for the year ahead, though their starting assumptions and methodologies differ.

- CBA predicts Melbourne property prices to rise +1.0 per cent over 2026.

- Westpac predicts Melbourne property prices to fall -4.0 per cent over 2026.

- NAB's published forecast is at the Victoria state level; it predicts dwelling prices to fall -0.3 per cent over the next 12 months across Victoria.

- ANZ predicts Melbourne property prices to fall -1.7 per cent over 2026.

The spread runs from Westpac at the pessimistic end, forecasting a -4.0 per cent fall, through to CBA at the optimistic end with a +1.0 per cent gain. ANZ's -1.7 per cent sits closer to Westpac than to CBA, while NAB's Victoria-level figure of -0.3 per cent sits near the midpoint of the range, though it covers the broader state and should not be read as a Melbourne-specific forecast. The gap between the two ends of the spread is five percentage points, which tells you how much genuine uncertainty remains in the Melbourne property market predictions for the rest of the year.

RBA cash rate forecast 2026

The RBA cash rate currently sits at 4.35 per cent. Three of the Big Four banks expect the next move to be a cut, though Westpac stands apart, forecasting further rises. That split means there is no clean consensus on the rate path from here, and the timing of any move varies considerably across the banks.

According to Canstar:

- ANZ predicts that we’ll see 25 basis point cuts in September and December of 2027, bringing the cash rate to 3.85% by the end of next year.

- CBA predicts that we’ll see 25 basis point cuts in May and August of 2027, bringing the cash rate to 3.85% by the third quarter of next year.

- NAB predicts that we’ll see 25 basis point cuts in June, September and December of 2027, bringing the cash rate to 3.60% by the end of next year.

- Westpac currently predicts two more 25 basis point hikes in August and September, bringing the cash rate to 4.85%.

What this means for the Melbourne market

At 4.35 per cent, the cash rate remains at a level that constrains how much Melbourne buyers can borrow relative to what they could access in the low-rate years of 2020 and 2021. In a city where the median house price sits at $948,482, even modest changes in the rate environment can shift borrowing capacity by tens of thousands of dollars, directly affecting what buyers can bid.

Westpac's divergent forecast adds a layer of uncertainty that matters most for buyers weighing their timing. If rates do rise further, as Westpac expects, the downside forecasts from ANZ and Westpac on dwelling values become more plausible. If the three-bank majority view of a cut eventuates, that could begin to ease the pressure that has weighed most heavily on Melbourne houses, while units, which have held better through this period of falling values, may respond more quickly to any improvement in sentiment.

NAB's forecasts predate the most recent RBA decision, so its rate and price views may be revised as more current data flows through.

Helpful resource: Our simple guide to tracking market trends and data will walk you through everything you need to know to be able to read the market and make a smarter selling decision.

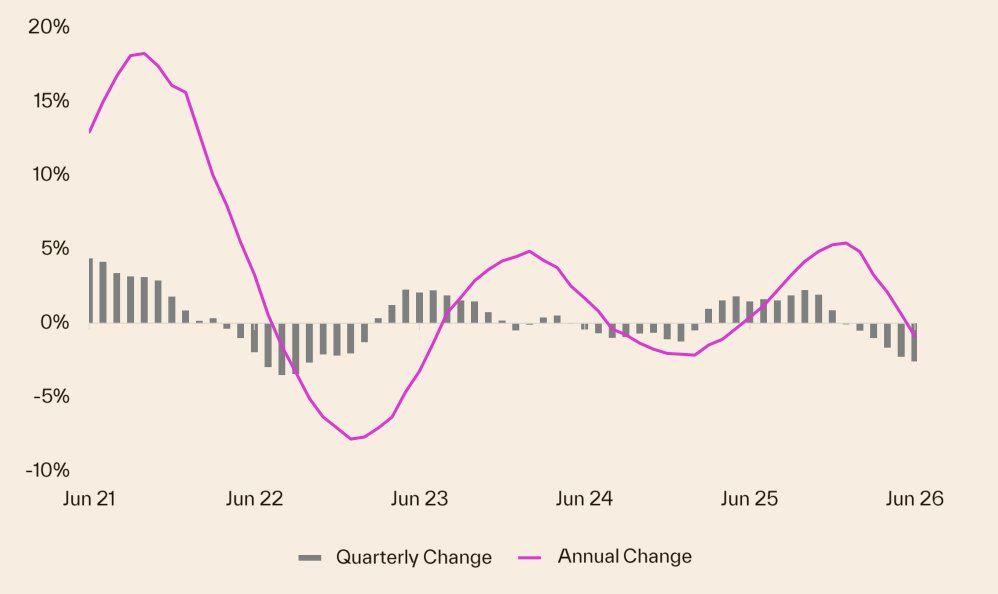

Melbourne house prices graphs and charts

Melbourne's house price growth over the last 5 years has moved through sharp swings, and according to Cotality's latest figures, dwelling values fell -1.0 per cent over the month to June 2026, -2.6 per cent over the quarter, and -0.9 per cent over the year, leaving the current dwelling median at $808,486. That places Melbourne -4.0 per cent below its March 2022 peak, meaning the city has given back a meaningful share of the gains made during the post-pandemic surge.

The five-year arc reflects the full force of the rate cycle: values climbed sharply through 2021 as borrowing costs hit historic lows, then pulled back as the Reserve Bank lifted the cash rate to 4.35 per cent across 2022 and 2023. Since late 2025, rising total listings, up +17.4 per cent on a year ago, combined with cautious buyer demand have kept downward pressure on prices, with the quarterly decline now the steepest Melbourne has recorded in several years.

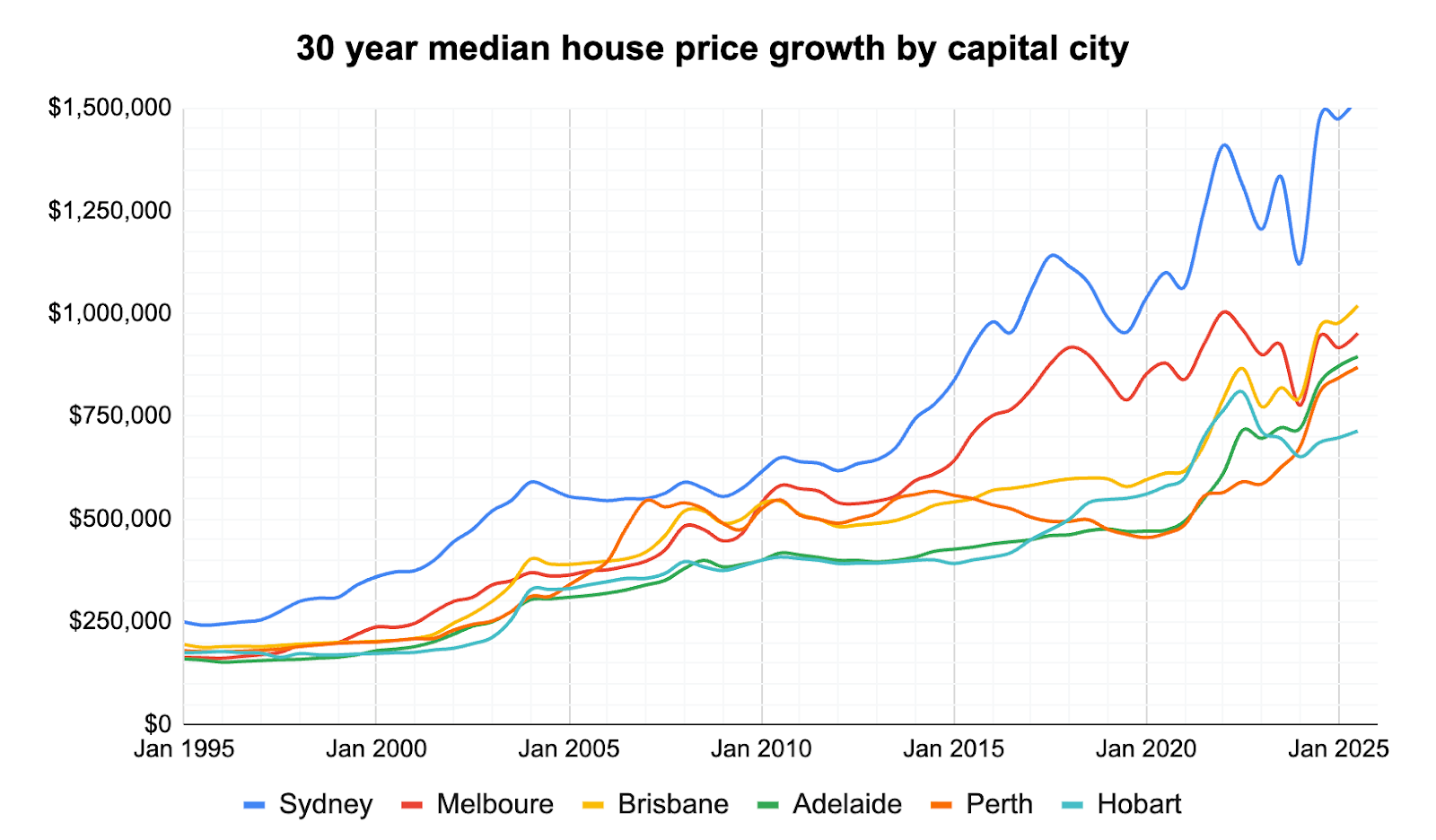

Melbourne property 30 year property price graph

This recent “slow grind” back toward prior highs sits alongside Melbourne property prices growth over the last 10 years, where strong long-run gains were driven by falling interest rates, population growth and constrained supply that together pushed the median much higher; OpenAgent’s historical review shows Melbourne’s median house price rising to roughly $1.1 million by 2025, reflecting that decade-plus of solid appreciation.

Over the past 30 years, Melbourne has repeatedly moved through booms and corrections, and today, homeowners are more cautious while still supported by tight rental markets and ongoing population inflows; supply shortfalls and construction constraints mean demand pressures remain, even as higher borrowing costs temper how fast prices can climb.

Melbourne selling statistics

Selling conditions in Melbourne are clearly weighted toward buyers right now. Stock has risen sharply, properties are sitting on the market longer than a year ago, and sellers are accepting offers further below their asking price than they were twelve months back.

Want to know what your own property is worth? Get a free value estimate for your address.

Melbourne sales volume and days on market

Melbourne recorded sales volume growth of +3.9 per cent year on year, a result that stands against a combined capitals average of -0.7 per cent and a national figure of +2.1 per cent. At the same time, the median days on market stretched to 36 days, up from 34 days a year ago.

| Melbourne sales volume | Melbourne days on market |

|---|---|

| +3.9% Change from 12mo ago | 36 days 34 days 12 mo ago |

Source: Cotality

Melbourne is selling more properties than it was a year ago, but it is taking longer to do so. The combined capitals median is 30 days and the national figure is 32 days, meaning Melbourne properties are spending roughly six days more on market than the average capital city home.

Melbourne new and total listings

New listings rose +4.3 per cent year on year, while total advertised listings climbed +17.4 per cent over the same period. That gap between new and total listings tells its own story: properties are accumulating on the market rather than clearing quickly.

| Melbourne new listings | Melbourne total listings |

|---|---|

| +4.3% Change from 12mo ago | +17.4% Change from 12mo ago |

Source: Cotality

For buyers, the rise in total stock means considerably more choice than a year ago. For sellers, it means more competition for buyer attention, and that additional competition has contributed to the softening in both prices and time on market seen across Melbourne over the June quarter.

Melbourne vendor discount and auction clearance rates

Vendor discount measures the percentage gap between a property's initial asking price and its eventual sale price, giving a read on how much sellers are adjusting their expectations to meet the market. Auction clearance rates measure the share of properties sold at auction in a given week. Together, the two figures show both the negotiating environment and the level of buyer competition at the sharp end of the sales process.

Melbourne vendor discount

| June 2026 | June 2025 | |

|---|---|---|

| Melbourne median vendor discount | -3.5% | -3.1% |

Source: Cotality

Melbourne's vendor discount widened to -3.5 per cent, compared with -3.1 per cent a year earlier. Sellers are accepting offers further below their asking price than they were twelve months ago, a shift consistent with the higher stock levels and softer demand the city has recorded through the June quarter.

Melbourne auction clearance rates

| Melbourne | 12 Jul 2026 |

|---|---|

| Total Auctions | 576 |

| Sold | 290 |

| Withdrawn | 68 |

| Passed in | 218 |

| Clearance Rate | 50.4% |

Source: Cotality

For the week ending 12 July 2026, Melbourne recorded a clearance rate of 50.4 per cent from 576 auctions, with 290 properties sold and 218 passed in. A clearance rate just above 50 per cent is a soft result by any measure, sitting well below the long-run decade average of around 64 per cent and placing conditions clearly in buyer-favourable territory.

Thinking of selling? Compare top-performing local agents in your suburb to find the right fit for your sale.

Get a deeper insight into how Melbourne sellers are faring in 2026 and what could be on the horizon for the year ahead with some of our latest articles.

Melbourne property investing

Melbourne's rental market continues to generate income for investors even as property values ease, with rents rising and yields sitting above those recorded in some larger capitals. For renters, conditions remain tight relative to historical norms, though Melbourne offers more breathing room than most other Australian cities.

Helpful resource: Estimate the capital gains tax on a sale with our free calculator.

Melbourne rental market

The table below covers annual rent growth, gross rental yield, and the breakdown of rental change for houses and units across Melbourne and the other capital cities. These figures give a picture of how Melbourne compares nationally for both rental income and investment return.

| Location | Rental rates | Rental yield | Annual change in rents, houses | Annual change in rents, units |

|---|---|---|---|---|

| National | 5.9% | 3.7% | NA | NA |

| Combined Capitals | 6.0% | 3.5% | NA | NA |

| Combined Regional | 5.9% | 4.2% | NA | NA |

| Sydney | 5.9% | 3.3% | 6.6% | 4.7% |

| Melbourne | 4.9% | 3.9% | 4.9% | 4.8% |

| Brisbane | 6.4% | 3.3% | 6.6% | 5.8% |

| Adelaide | 4.8% | 3.5% | 4.9% | 4.3% |

| Perth | 7.8% | 3.7% | 7.9% | 7.6% |

| Hobart | 8.6% | 4.4% | 9.1% | 6.6% |

| Darwin | 10.1% | 6.1% | 10.8% | 9.0% |

| Canberra | 3.2% | 4.2% | 3.9% | 1.7% |

Source: Cotality

Melbourne rents rose +4.9 per cent over the year to June 2026, with houses and units both lifting at a similar pace. The rental yield of 3.9 per cent sits above Sydney and Brisbane, the two most expensive capital city markets, suggesting Melbourne's relative value position is working in investors' favour as purchase prices ease.

Melbourne's yield recovery reflects the dual effect of rising rents and softening property values. For investors focused on income return rather than short-term capital growth, the current environment is meaningfully different to 2022, when yields were considerably lower.

Melbourne vacancy rates

Vacancy rates measure the share of rental properties sitting empty at any given time, and they are one of the most direct signals of rental demand pressure. SQM data shows that Melbourne's vacancy rate has moved over the past year, providing context for how much choice renters have and how quickly landlords can expect to fill a property.

| Location | June 2026 vacancy rates | June 2026 vacancies | June 2025 vacancy rates | June 2025 vacancies |

|---|---|---|---|---|

| National | 1.3% | 39,229 | 1.3% | 39,027 |

| Sydney | 1.6% | 11,957 | 1.6% | 11,482 |

| Melbourne | 1.6% | 8,640 | 1.8% | 9,414 |

| Brisbane | 0.9% | 3,065 | 0.9% | 3,147 |

| Adelaide | 0.7% | 1,096 | 0.8% | 1,268 |

| Perth | 0.6% | 1,247 | 0.8% | 1,457 |

| Hobart | 0.7% | 185 | 0.6% | 175 |

| Darwin | 0.3% | 64 | 0.5% | 115 |

| Canberra | 1.7% | 1,063 | 1.5% | 920 |

Source: SQM Research

Melbourne's vacancy rate fell from 1.8 per cent a year ago to 1.6 per cent, with the number of vacant properties dropping from 9,414 to 8,640. That is a meaningful tightening over twelve months, and it places Melbourne alongside Sydney as the loosest of the capital markets, though both remain well above the sub-1 per cent rates seen in Brisbane, Adelaide and Perth.

At 1.6 per cent, Melbourne is the most balanced rental market among the major capitals. The gap between Melbourne and cities like Perth (0.6 per cent) and Adelaide (0.7 per cent) is significant: renters have more options here, and landlords face more competition when a property comes to market.

Louis Christopher, Managing Director at SQM Research said in the latest rental market report:

"While the national vacancy rate has edged up to 1.3%, Australia's rental market remains exceptionally tight by historical standards. Most capital cities continue to record vacancy rates below one per cent or only marginally above, highlighting that rental supply remains insufficient to meet demand."

Melbourne sits above the national average vacancy rate, but the broader supply shortfall described in that observation is still relevant here. Melbourne's vacancy rate has tightened over the past year even from a relatively more available base, suggesting demand continues to absorb any incremental supply that comes to market. For investors, a vacancy rate that is falling while rents are rising points to a rental market that continues to favour landlords over the medium term, even if Melbourne is not as supply-constrained as other capitals.

Highest growth areas in Melbourne

Melbourne's strongest annual price gains in June 2026 were concentrated in the city's outer and middle-ring corridors, where relative affordability continues to draw steady buyer interest. The table below ranks the top 10 Statistical Area Level 3 (SA3) regions across Greater Melbourne by annual percentage change, an SA3 is an Australian Bureau of Statistics classification that typically groups several adjacent suburbs into a single geographic area.

| Rank | SA3 Name | SA4 Name | Median Value | Annual % Change |

|---|---|---|---|---|

| 1 | Sunbury | North West | $740,158 | 5.4% |

| 2 | Brimbank | West | $729,767 | 4.9% |

| 3 | Casey - South | South East | $808,354 | 4.6% |

| 4 | Frankston | Mornington Peninsula | $819,555 | 3.7% |

| 5 | Keilor | North West | $1,035,611 | 3.5% |

| 6 | Casey - North | South East | $860,657 | 3.4% |

| 7 | Cardinia | South East | $779,113 | 3.3% |

| 8 | Tullamarine - Broadmeadows | North West | $731,262 | 3.2% |

| 9 | Maribyrnong | West | $676,667 | 3.0% |

| 10 | Melton - Bacchus Marsh | West | $670,014 | 2.8% |

Source: Cotality

Highlights for Melbourne’s high growth areas

- Sunbury: Ranked #1 with annual growth of +5.4 per cent and a median value of $740,158, Sunbury is Melbourne's top-performing SA3 for the year to June 2026. The region sits in the city's far north-west and offers buyers a combination of relative affordability and improving infrastructure links, with suburbs such as Diggers Rest and Sunbury drawing consistent interest from families and first-home buyers looking beyond the middle ring.

- Brimbank: Ranked #2 with +4.9 per cent annual growth and a median value of $729,767, Brimbank covers a broad swathe of Melbourne's inner-west. Its entry-level price point relative to comparable distances from the city centre has supported purchasing activity, with suburbs such as St Albans and Sunshine West among the more active pockets in the region.

- Casey - South: Ranked #3 with +4.6 per cent annual growth and a median value of $808,354, Casey - South sits in Melbourne's outer south-east and has benefited from ongoing residential development and population growth. Suburbs such as Clyde North and Cranbourne East have been at the centre of that activity, attracting buyers seeking newer housing stock at prices below the city median.

- Frankston and Keilor: Ranks #4 and #5, Frankston (+3.7 per cent, $819,555) and Keilor (+3.5 per cent, $1,035,611), represent two quite different but similarly performing markets. Frankston, on the Mornington Peninsula fringe, draws buyers with coastal access and relative affordability, with suburbs such as Seaford and Langwarrin popular among families; Keilor, sitting in the north-west, appeals at a higher price point with suburbs such as Strathmore offering more established streetscapes closer to the city.

- South-east and north-west growth band: Ranks #6 through #8, Casey - North (+3.4 per cent, $860,657), Cardinia (+3.3 per cent, $779,113), and Tullamarine - Broadmeadows (+3.2 per cent, $731,262), form a broad arc of outer-suburban growth. Casey - North includes established suburbs such as Berwick and Narre Warren; Cardinia covers growing communities such as Pakenham and Officer further south-east; and Tullamarine - Broadmeadows, anchored by suburbs including Craigieburn, continues to attract buyers drawn by new housing supply and transport access in Melbourne's north-west.

Thinking of selling or investing in Melbourne? Compare local agents or get a free property report with OpenAgent.

View agent & property tools

Our powerful property tools