Changing conditions see some markets flatline, others soar in December

2021 was a year filled with drama both inside and outside of the real estate sphere. It's fitting, then, that CoreLogic's latest report brings one last twist for the property market in December.

On a national level, +1.0 per cent gains for the month brought total annual growth up to +22.1 per cent. But now, after a period of easing, some markets are pushing further ahead and setting new records for the cycle while others have pulled right back.

It all sets the stage for a fascinating first quarter of 2022 for Australian property.

National property values: December 2021

| Houses | Units |

|---|---|

| $766,377 | $602,933 |

| Monthly change: +1.2% | Monthly change: +0.4% |

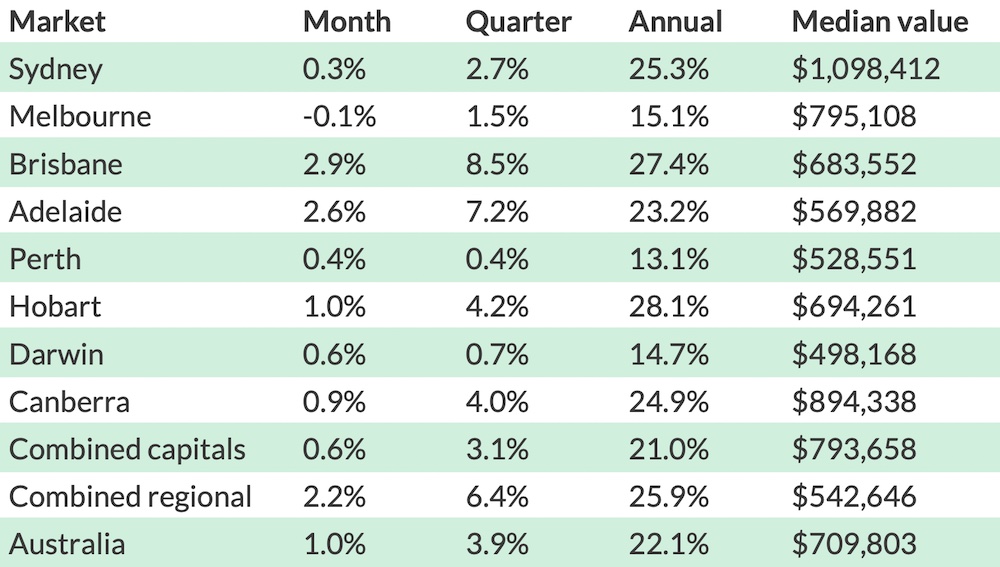

The +1.0 per cent boost to dwelling prices across the country has nudged the national median home value up to $709,803 to start the new year.

Breaking things down across the capital and regional markets, though, shows a very diverse picture.

The country's two most populous markets both saw a big drop in momentum in December. Sydney price growth declined sharply to just +0.3 per cent for the month, while Melbourne saw a drop of -0.1 per cent, the first fall since October 2020.

Hobart and Canberra, both major growth cities in 2021, remained more steady for the month, sitting at around the +1.0 per cent mark.

Perth and Darwin also saw some modest growth after both flatlining over the previous quarter.

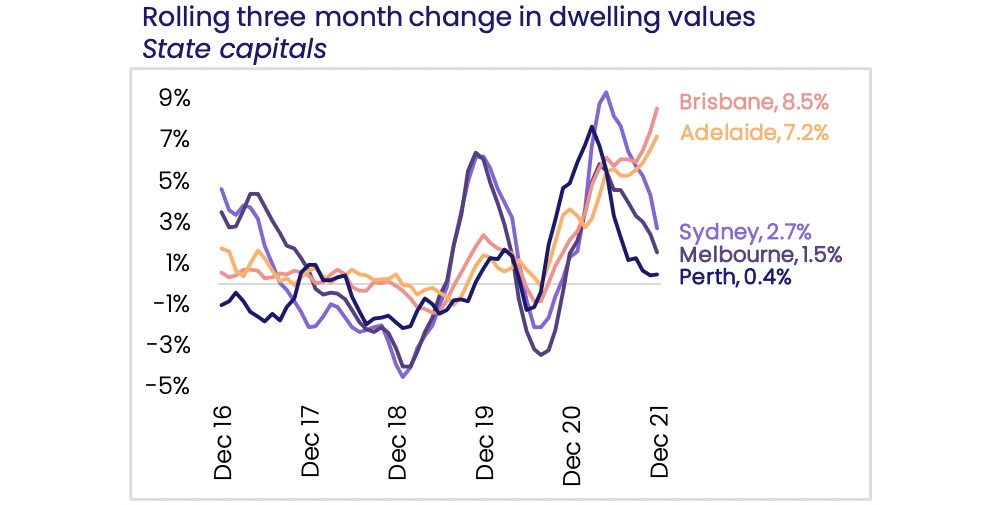

The story completely flips when looking at Brisbane and Adelaide, though.

After delivering their highest growth rates for the year in November, both cities surged ahead for another mammoth month. Brisbane prices shot up another +2.9 per cent, while Adelaide values got another huge +2.6 per cent boost.

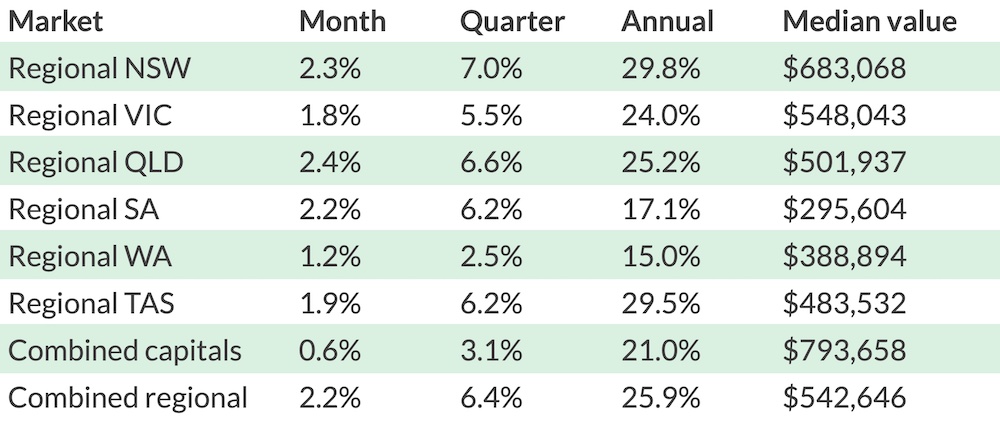

Regional markets also continued their strong run, with December's +2.2 per cent bump representing their highest gains in nine months.

Even with conditions easing in a number of the capitals, the year wraps up with incredibly strong gains seen across the board, with five cities posting well above +20 per cent annual growth.

Multi-speed markets now seeing momentum shifts in both directions

Where earlier in 2021 there was relatively uniform growth being seen across all the capital cities, we're now seeing the numbers telling distinctly different stories between state lines.

Speaking to the new highs in Brisbane and Adelaide, CoreLogic's research director Tim Lawless explains that "these regions show less of an affordability challenge relative to the larger capitals, as well as better support for housing demand with Queensland in particular showing strong interstate migration."

He adds that advertised stock on the market remains "remarkably low" in the two cities, meaning demand continues to significantly outstrip supply.

The opposite dynamic is at play in Melbourne and Sydney especially.

"A surge in freshly advertised listings through December has been a key factor in taking some heat out of the Melbourne and Sydney housing markets, along with some demand headwinds caused by significant affordability constraints and negative interstate migration," Mr Lawless says.

Those conditions have led some experts to call the peak of the market in most areas of Australia. While Brisbane and Adelaide may experience more strong gains in this cycle, it's expected that the other capitals will continue to see a softening in price growth moving forward.

Regional markets continue their renewed upward trend

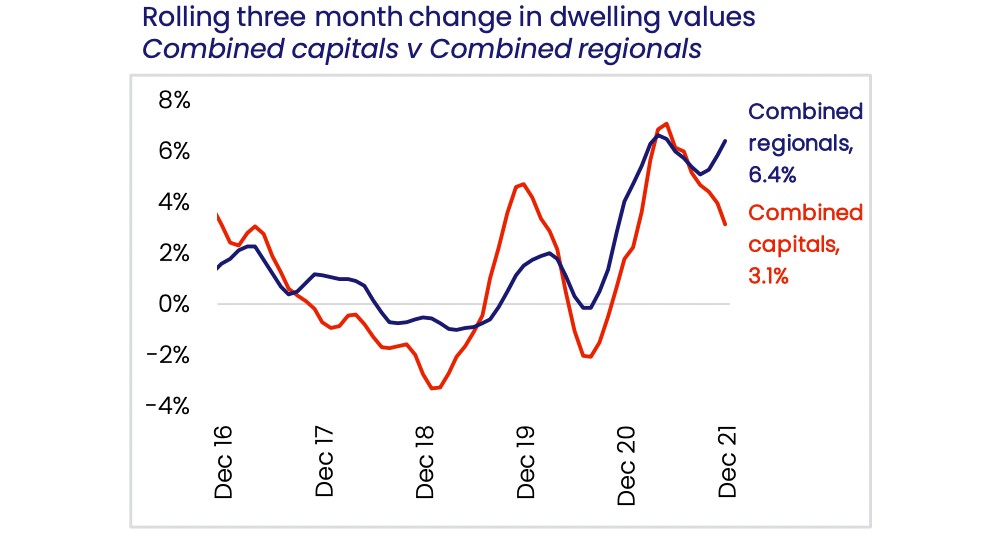

CoreLogic notes that regional property values are up +32 per cent since March 2020 relative to a +20 per cent uptick across the capitals over the same period.

After regional growth began to slow at roughly the same rate as the capitals midway through 2021, it's shot back up over the past quarter. Over that three-month period, regional prices have grown at more than double the rate that they have in capital cities.

The report explains that this could be reflective of a fresh wave of demand, particularly since Sydney and Melbourne buyers emerged from lockdowns.

Available stock on the market in regional areas remains on the whole far lower (-35.9 per cent) than the five-year average when compared to the capital cities, so it's a similar situation to Brisbane and Adelaide where the supply and demand balance remains very favourable to sellers.

Locations with lifestyle appeal, particularly coastal areas, have remained highly desirable as flexible working policies continue and international travel restrictions push demand for holiday homes.

CoreLogic notes that, despite the continued regional gains, the growing issue of affordability combined with potential interest rate rises mean regional markets "may also move into a downswing phase over the course of 2022."

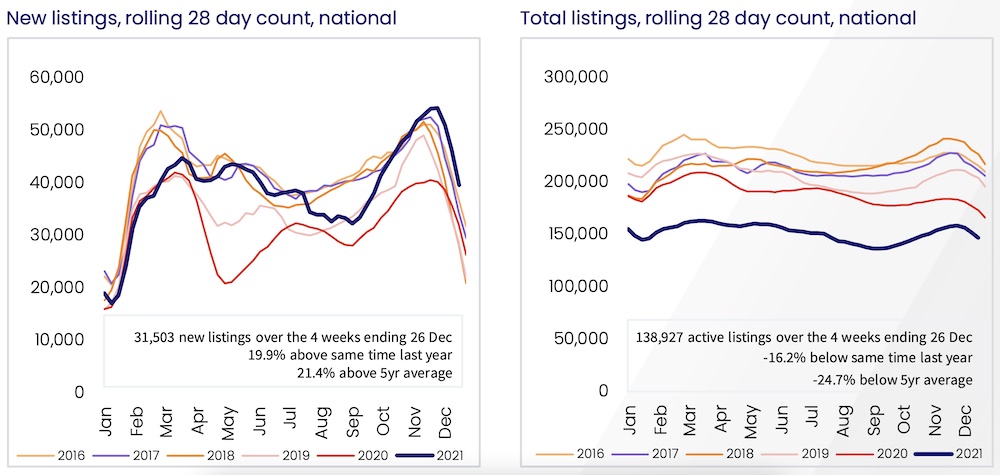

Total listings remain below average, but different markets tell different stories

A defining feature of the 2021 property boom was low levels of available stock creating a highly competitive environment for buyers. While stock levels remain low on a national level, that story changes when looking at the city level.

The slowdown or acceleration of price growth correlates to the number of new listings that have come to the market in recent months. In Sydney and Melbourne, total stock levels are close to the five-year average.

CoreLogic notes that "the number of new listings added to the Australian housing market through December was +21.4 per cent above the five-year average, demonstrating vendor confidence amidst quick selling times and high auction clearance rates."

In Brisbane and Adelaide, total listings are still around -35 per cent down from the five-year average, and that's a key factor in the continued surge in growth.

Looking at 2021 as a whole, CoreLogic estimates more than 650,000 properties changed hands for the year. That's the highest number of annual sales on record.

Mr Lawless says that "as stock levels normalise and affordability constraints along with tighter credit conditions drag down demand, it's reasonable to expect growth conditions will be more subdued in 2022."

What's next for the Australian property market?

Looking ahead to the coming months, CoreLogic point out a number of headwinds that could continue to curb price growth.

Affordability remains one of the core drivers of the slowdown in most markets. That won't be helped by the potential for interest rates to rise as early as late 2022, and there is still the potential for further tightening to housing credit policies.

Outside of Brisbane, Adelaide and some of the regional markets, stock levels are balancing out with demand, which may further ease gains.

The upcoming federal election may also come into play. Typically, elections slow property market activity temporarily until a result is known, and issues around home ownership and housing affordability will be key talking points.

Then, of course, there is the great unknown of how the ongoing Omicron outbreak will impact the property market and the wider economy.

On the other hand, immigration is still set to ramp back up this year, and interest rates, even if they do rise, will remain close to their lowest levels in history. Prices should continue to rise as 2022 unfolds, just at a more moderate rate than the previous year.

In the short term, CoreLogic expects more diversity between different cities and markets, as we've already seen in the December growth figures.

Overall, it's forecast that we'll see a more 'normal' year for real estate, with supply and demand balancing out, clearance rates holding around average levels and homes selling less rapidly.

It's important to remember that every market is different, as is every property. If you're considering selling, speaking to a top agent in your local area is often the best first step towards getting a full picture of what's going on around you and where the market might be heading.