- https://sketchapp.com --%3e %3ctitle%3eIcon/search%3c/title%3e %3cdesc%3eCreated with Sketch.%3c/desc%3e %3cg id='Icon/search' stroke='none' stroke-width='1' fill='none' fill-rule='evenodd' stroke-linecap='round' stroke-linejoin='round'%3e %3ccircle id='Oval' stroke='%23252525' cx='10.5145111' cy='10.5145111' r='6.99455261'%3e%3c/circle%3e %3cpath d='M15.4908752%2c15.4908752 L20.5515137%2c20.5515137' id='Line' stroke='%23252525'%3e%3c/path%3e %3c/g%3e%3c/svg%3e)

Perth property market news - key takeaways

- Perth property market at record highs: Perth dwelling values rose +0.7 per cent in June 2026, reaching a median of $1,046,551, with annual growth of +23.9 per cent placing the city at a record high and well ahead of every other capital.

- Listings rising but supply still tight: Total listings climbed +16.7 per cent year on year, yet homes are still selling in a median of just 14 days, roughly half the time it takes to sell in the combined capitals.

- Sellers holding firm: Perth's vendor discount sits at -3.4 per cent, modest by national standards, meaning well-priced properties are still achieving close to asking price despite a slight widening over the past year.

- Rental demand outpacing supply: Perth's vacancy rate fell to 0.6 per cent, less than half the national figure, with annual rent growth of +7.8 per cent running well above the combined capitals average.

- Rate outlook split among major banks: Three of the four major banks forecast the next cash-rate move to be a cut, though not before mid-2027, while Westpac expects further rises from August, leaving the rate path genuinely uncertain for Perth buyers.

Get a free property value estimate

Find out how much your property is worth in today’s market.

Perth property price movements

The Perth property market has continued to set the pace nationally, with values climbing across all property types in June 2026. While much of the country has softened over recent months, Perth stands apart as one of the few major capitals still recording broad-based gains.

Perth property prices - June 2026

Perth's property market posted another solid result in June 2026, with the typical home value rising +0.7 per cent over the month. Quarterly growth of +2.0 per cent and an annual gain of +23.9 per cent place Perth well clear of every other capital city.

| Property type | Current median price | Monthly change | Quarterly change | Annual change |

|---|---|---|---|---|

| All Perth dwellings | $1,046,551 | +0.7% | +2.0% | +23.9% |

Source: Cotality

The median value across Perth properties reached $1,046,551, adding around $7,279 over the month. Perth values are at a record high.

House prices in Perth

Perth house prices rose +0.7 per cent in June 2026, with the median now sitting at $1,093,431. The Perth housing market has delivered annual growth of +23.6 per cent, meaning the typical house is worth significantly more than it was just twelve months ago.

| Property type | Current median price | Monthly change | Quarterly change | Annual change |

|---|---|---|---|---|

| Perth houses | $1,093,431 | +0.7% | +1.9% | +23.6% |

Source: Cotality

That monthly gain translates to an increase of around $7,613 in the median house value. Houses have slightly outpaced the broader market on an annual basis, though units have pulled ahead over shorter timeframes.

Unit prices in Perth

Perth unit prices edged higher again in June 2026, rising +0.8 per cent over the month to a median of $773,605. Annual growth of +26.3 per cent means Perth unit prices have been the stronger performer across both the monthly and annual measures compared with houses.

| Property type | Current median price | Monthly change | Quarterly change | Annual change |

|---|---|---|---|---|

| Perth units | $773,605 | +0.8% | +3.0% | +26.3% |

Source: Cotality

The monthly gain added around $6,143 to the typical unit's value. The stronger annual growth rate for units suggests demand has been particularly strong at the more accessible end of the Perth market, where entry prices remain below the house segment.

Perth property market forecasts 2026

Australia's Big Four banks publish annual dwelling price forecasts as part of their economic research divisions, and views on Perth for 2026 span a wide range. Each bank applies its own methodology and horizon, so the figures below reflect genuine differences in outlook rather than data discrepancies.

- CBA predicts Perth property prices to rise +15.0 per cent over 2026.

- Westpac predicts Perth property prices to rise +13.0 per cent over 2026.

- NAB's published forecast is at the Western Australia state level; it predicts dwelling prices to rise +5.5 per cent over the next 12 months across Western Australia.

- ANZ predicts Perth property prices to rise +12.3 per cent over 2026.

CBA holds the most optimistic Perth house price forecast at +15.0 per cent, while NAB's Western Australia state figure of +5.5 per cent sits at the other end of the spread. Because NAB's figure covers the broader state rather than Perth specifically, a direct comparison with the city-level forecasts should be treated with some caution. Among the three city-level Perth property market predictions, ANZ's +12.3 per cent sits closest to Westpac's +13.0 per cent, with CBA a step above both.

RBA cash rate forecast 2026

The RBA cash rate currently sits at 4.35 per cent. Three of the four major banks expect the next move to be a cut, though Westpac stands apart, forecasting rate rises rather than reductions from here.

According to Canstar:

- ANZ predicts that we’ll see 25 basis point cuts in September and December of 2027, bringing the cash rate to 3.85% by the end of next year.

- CBA predicts that we’ll see 25 basis point cuts in May and August of 2027, bringing the cash rate to 3.85% by the third quarter of next year.

- NAB predicts that we’ll see 25 basis point cuts in June, September and December of 2027, bringing the cash rate to 3.60% by the end of next year.

- Westpac currently predicts two more 25 basis point hikes in August and September, bringing the cash rate to 4.85%.

What this means for the Perth market

At 4.35 per cent, the cash rate remains at a level that adds meaningful pressure to borrowing costs. For Perth buyers, particularly those stretching to meet the city's record-high median of $1,046,551, the current rate environment constrains how much most households can borrow relative to two or three years ago.

The split between the banks on the rate path matters for how quickly that pressure eases. If the majority view of gradual cuts from mid-to-late 2027 proves correct, some relief on serviceability may arrive within the forecast window, though the timing still sits 12 months or more away. Westpac's divergent forecast of further rises, if realised, would extend affordability pressure and could put the upper end of the bank price forecasts under strain.

Units may prove more resilient to rate sensitivity than houses in this environment, given their lower absolute price point. Perth's +12.3 to +15.0 per cent city-level forecast range assumes conditions broadly supportive of continued demand, which a further rate rise scenario would test.

NAB's forecast draws on a Q1 2026 research horizon, so its views on the Western Australia market may be revised as 2027 rate expectations firm.

Helpful resource: Our simple guide to tracking market trends and data will walk you through everything you need to know to be able to read the market and make a smarter selling decision.

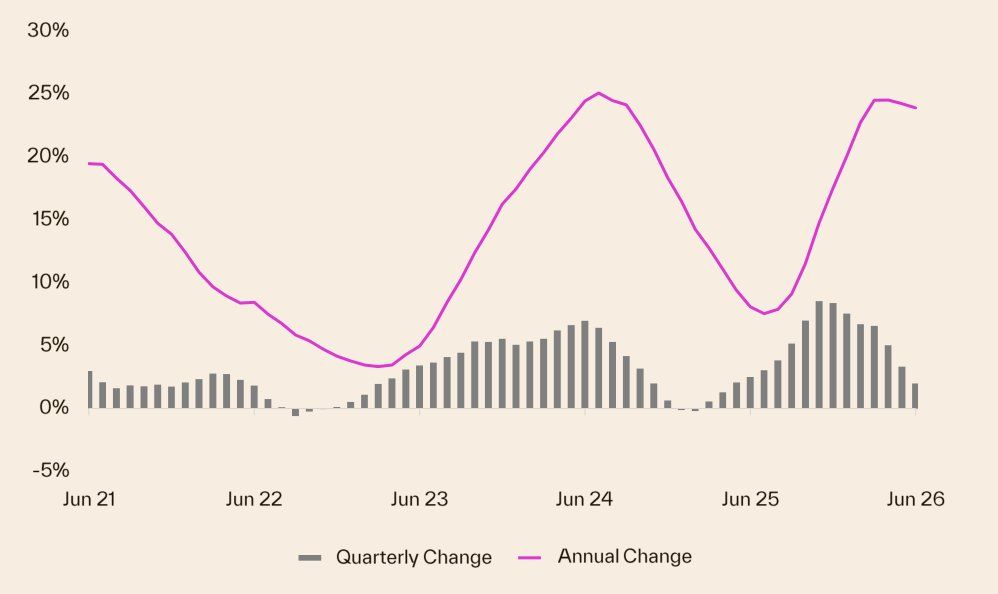

Perth house prices graphs and charts

Perth's house price growth over the last 5 years has continued to outpace every other Australian capital, with dwelling values rising +0.7 per cent in June, +2.0 per cent over the quarter, and +23.9 per cent over the year to a median of $1,046,551, according to Cotality's latest figures. Perth is currently at a record high, making it one of only two capital cities still posting positive monthly and quarterly gains at a time when most other capitals have pulled back.

The five-year run of growth has been shaped by a combination of tight housing supply, strong interstate and overseas migration, and an entry price point that remains well below Sydney and Melbourne, all of which have kept buyer demand ahead of available stock. While the cash rate held at 4.35 per cent through this period weighed on borrowing capacity nationally, Perth's relative affordability helped sustain purchasing activity even as conditions softened elsewhere, with homes selling in a median of just 14 days compared with 30 days across the combined capitals.

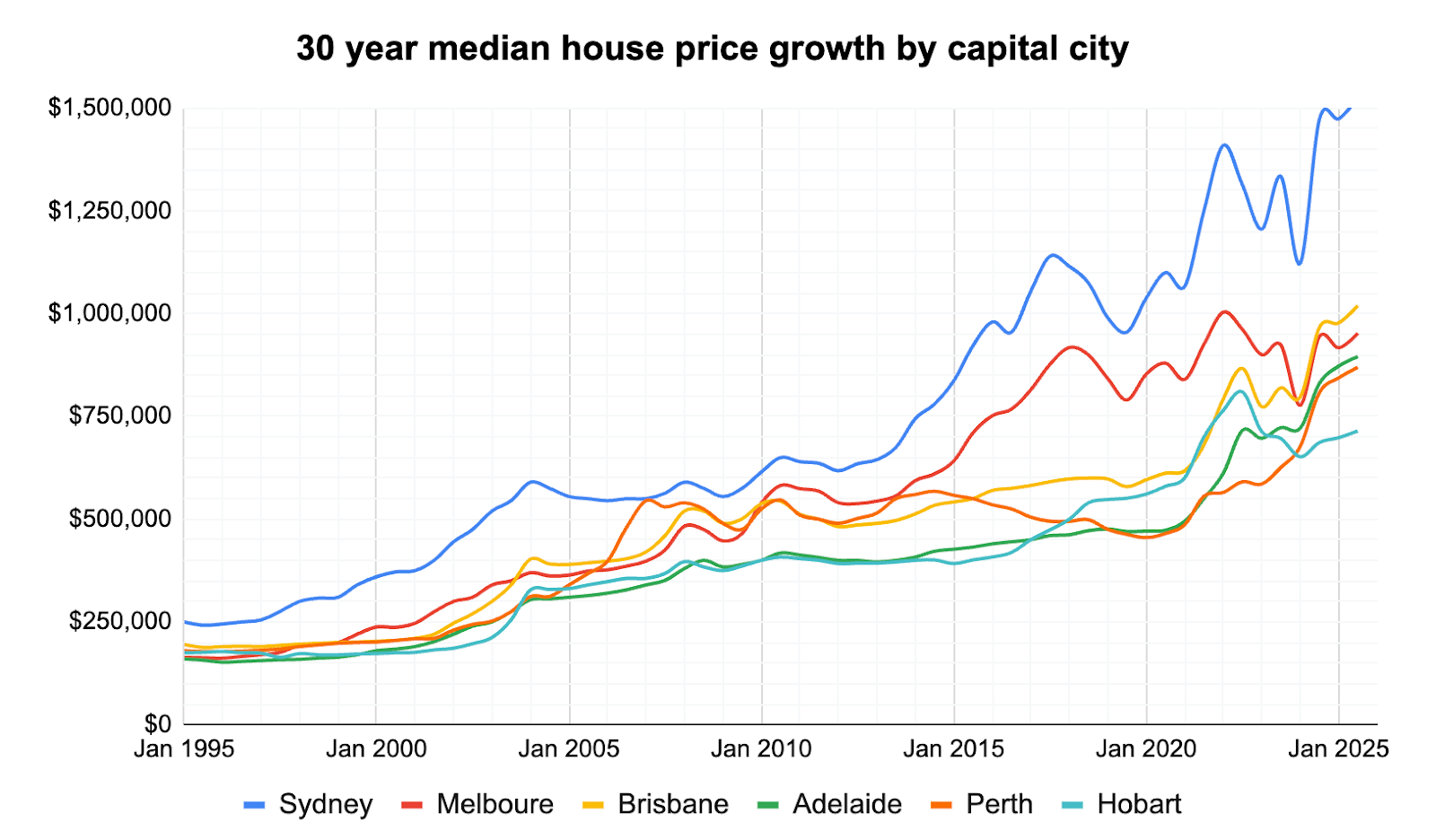

Perth property 30 year property price graph

Recent gains sit on top of a long, cyclical history where booms and busts have tended to follow the state’s resource cycles, so Perth property prices growth over the last 10 years has been uneven — a long slump after the 2014 peak was followed by a powerful recovery and the current run to new highs around the $960,000 median range.

Over three decades, the market has been driven by shifting mining fortunes, changing population flows and periods of under-building that later tightened supply. Today, those same forces — stronger population growth, very low vacancy rates and limited new listings — are supporting prices. Homeowners are generally feeling more confident after recent gains, while buyers report frustration and urgency because higher repayments and scarce stock make finding and affording a home harder right now.

Perth selling statistics

Perth's property market continues to run at a pace well ahead of the national average. Selling conditions here look markedly different from most other capitals, with homes moving quickly and supply, though growing, still constrained relative to demand.

Want to know what your own property is worth? Get a free value estimate for your address.

Perth sales volume and days on market

Sales volume in Perth fell -13.8 per cent year on year, a notable pullback compared with the combined capitals average of -0.7 per cent and the national figure of +2.1 per cent. Properties are selling in a median of 14 days, unchanged from a year ago, and roughly half the time of the combined capitals (30 days) and the national median (32 days).

| Perth sales volume | Perth days on market |

|---|---|

| -13.8% Change from 12mo ago | 14 days 14 days 12 mo ago |

Source: Cotality

Perth's 14-day selling time is the fastest of any capital city in the country. The volume decline alongside that speed tells a clear story: there are fewer transactions, but the ones that do happen are resolving quickly, which points to strong intent among buyers who do engage.

Perth new and total listings

New listings rose +14.3 per cent year on year, and total listings climbed +16.7 per cent over the same period. Both figures reflect a market where more sellers are choosing to test conditions, adding to a stock base that was exceptionally thin throughout 2024 and 2025.

| Perth new listings | Perth total listings |

|---|---|

| +14.3% Change from 12mo ago | +16.7% Change from 12mo ago |

Source: Cotality

Even with the uplift in supply, Perth's total listing levels remain low compared with historical norms and with the larger eastern-capital markets. Buyers have more choice than a year ago, but the pool of available homes is still relatively shallow, which continues to support asking prices and limit negotiating room.

Perth vendor discount

Vendor discount measures the percentage difference between a property's initial asking price and its final sale price. A wider discount means sellers are accepting offers further below what they initially listed for, while a narrower discount means the gap between asking and achieved prices is smaller. Weekly auction clearance rates are not included for Perth because auction volumes are too low to be statistically meaningful.

| June 2026 | June 2025 | |

|---|---|---|

| Perth median vendor discount | -3.1% | -3.1% |

Source: Cotality

Perth's vendor discount stood at -3.4 per cent in June 2026, compared with -3.0 per cent a year earlier. The gap has widened modestly, meaning sellers are, on average, accepting offers slightly further below their initial asking prices than they were 12 months ago. That said, -3.4 per cent remains modest relative to markets like Sydney, and the figure reflects conditions that still favour a well-priced listing.

Thinking of selling? Compare top-performing local agents in your suburb to find the right fit for your sale.

Get a deeper insight into how Perth sellers are faring in 2026 and what could be on the horizon for the remainder of the year with some of our latest articles.

Perth property investing

Perth's rental market continues to run hot for investors, with rents rising well above the national pace and vacancy conditions among the tightest of any capital city in the country. For renters, that means finding and keeping a property remains genuinely difficult.

Helpful resource: Estimate the capital gains tax on a sale with our free calculator.

Perth rental market

The table below covers Perth's annual rental growth, gross rental yield, and how rent changes for houses and units compare against other capitals and national benchmarks.

| Location | Rental rates | Rental yield | Annual change in rents, houses | Annual change in rents, units |

|---|---|---|---|---|

| National | 5.9% | 3.7% | NA | NA |

| Combined Capitals | 6.0% | 3.5% | NA | NA |

| Combined Regional | 5.9% | 4.2% | NA | NA |

| Sydney | 5.9% | 3.3% | 6.6% | 4.7% |

| Melbourne | 4.9% | 3.9% | 4.9% | 4.8% |

| Brisbane | 6.4% | 3.3% | 6.6% | 5.8% |

| Adelaide | 4.8% | 3.5% | 4.9% | 4.3% |

| Perth | 7.8% | 3.7% | 7.9% | 7.6% |

| Hobart | 8.6% | 4.4% | 9.1% | 6.6% |

| Darwin | 10.1% | 6.1% | 10.8% | 9.0% |

| Canberra | 3.2% | 4.2% | 3.9% | 1.7% |

Source: Cotality

Perth's annual rental growth of +7.8 per cent sits comfortably above the combined capitals average of +6.0 per cent, placing it third among capital cities behind only Darwin and Hobart. The gross yield of 3.7 per cent matches the national figure and sits ahead of Sydney and Brisbane, both at 3.3 per cent, reflecting Perth's position as a market where strong value growth has not entirely outpaced income returns. Both houses and units are tracking closely, with houses up +7.9 per cent and units up +7.6 per cent, suggesting rental demand is broad-based rather than concentrated in one dwelling type.

Perth vacancy rates

Vacancy rates measure the share of rental properties sitting empty at any given time. A low rate signals that demand from tenants is outpacing available supply, which puts upward pressure on rents. SQM data shows that Perth's vacancy rate has tightened over the past year, falling from 0.8 per cent to 0.6 per cent.

| Location | June 2026 vacancy rates | June 2026 vacancies | June 2025 vacancy rates | June 2025 vacancies |

|---|---|---|---|---|

| National | 1.3% | 39,229 | 1.3% | 39,027 |

| Sydney | 1.6% | 11,957 | 1.6% | 11,482 |

| Melbourne | 1.6% | 8,640 | 1.8% | 9,414 |

| Brisbane | 0.9% | 3,065 | 0.9% | 3,147 |

| Adelaide | 0.7% | 1,096 | 0.8% | 1,268 |

| Perth | 0.6% | 1,247 | 0.8% | 1,457 |

| Hobart | 0.7% | 185 | 0.6% | 175 |

| Darwin | 0.3% | 64 | 0.5% | 115 |

| Canberra | 1.7% | 1,063 | 1.5% | 920 |

Source: SQM Research

Perth's vacancy rate of 0.6 per cent is less than half the national figure of 1.3 per cent, and the available pool of 1,247 vacant properties is down from 1,457 a year ago. That tightening, from 0.8 per cent to 0.6 per cent over the year, tells a clear story: rental supply has not kept pace with demand. Among the capitals, only Darwin records a lower vacancy rate.

Louis Christopher, Managing Director at SQM Research said in the latest rental market report:

"While the national vacancy rate has edged up to 1.3%, Australia's rental market remains exceptionally tight by historical standards. Most capital cities continue to record vacancy rates below one per cent or only marginally above, highlighting that rental supply remains insufficient to meet demand."

Perth sits squarely in the picture Mr Christopher describes, with a vacancy rate of just 0.6 per cent placing it among the most supply-constrained markets in the country. For investors, that sustained tightness supports both continued rental growth and low vacancy risk. For renters, constrained supply means competition for available properties is unlikely to ease materially in the near term without a meaningful lift in new rental stock coming to market.

Highest growth areas in Perth

Perth's strongest annual price gains in June 2026 came from the city's outer southern and south-eastern corridors, with the city's northern and coastal fringes also featuring prominently. The table below ranks the top 10 Statistical Area Level 3 (SA3) regions across Greater Perth by annual percentage change, an SA3 is an Australian Bureau of Statistics classification that typically groups several adjacent suburbs into a single statistical region.

| Rank | SA3 Name | SA4 Name | Median Value | Annual % Change |

|---|---|---|---|---|

| 1 | Serpentine - Jarrahdale | South East | $980,075 | 30.8% |

| 2 | Armadale | South East | $927,293 | 29.4% |

| 3 | Rockingham | South West | $937,809 | 27.8% |

| 4 | Swan | North East | $963,270 | 27.7% |

| 5 | Mandurah | Mandurah | $914,467 | 26.5% |

| 6 | Kwinana | South West | $836,505 | 26.2% |

| 7 | Gosnells | South East | $932,736 | 26.1% |

| 8 | Wanneroo | North West | $1,008,406 | 26.0% |

| 9 | Cockburn | South West | $1,138,515 | 25.9% |

| 10 | Belmont - Victoria Park | South East | $1,036,717 | 25.6% |

Source: Cotality

Highlights for Perth’s high growth areas

- Serpentine - Jarrahdale: Ranked #1 across Greater Perth with annual growth of +30.8 per cent and a median value of $980,075, Serpentine - Jarrahdale has attracted steady buyer interest from households seeking more space and relative value at Perth's south-eastern fringe. Suburbs such as Byford have drawn particular attention as infrastructure investment in the corridor continues to support accessibility to the broader metro area.

- Armadale: Ranked #2 with annual growth of +29.4 per cent and a median of $927,293, Armadale sits at one of Perth's most affordable entry points within the south-eastern corridor and has seen demand supported by younger buyers and investors drawn by its price point relative to inner suburbs. Suburbs such as Harrisdale and Piara Waters have been among the busier pockets within the region.

- Rockingham: Ranked #3 with +27.8 per cent annual growth and a median of $937,809, Rockingham offers coastal lifestyle appeal combined with a median value that remains accessible by Perth standards. Suburbs such as Baldivis and Secret Harbour have attracted families seeking space and proximity to the coast south of the city.

- Outer south and south-west affordability corridor: Ranks #4 through #6, Swan (+27.7 per cent, $963,270), Mandurah (+26.5 per cent, $914,467) and Kwinana (+26.2 per cent, $836,505), each sit in Perth's outer ring, where relatively lower entry prices have continued to draw demand from buyers moving away from the city's middle and inner suburbs. Swan suburbs such as Ellenbrook and Aveley have seen consistent activity, while Mandurah's coastal location adds lifestyle appeal for buyers willing to commute or work remotely.

- South-east to north-west sweep: Ranks #7 through #10, Gosnells (+26.1 per cent, $932,736), Wanneroo (+26.0 per cent, $1,008,406), Cockburn (+25.9 per cent, $1,138,515) and Belmont - Victoria Park (+25.6 per cent, $1,036,717), span Perth from the south-east to the northern coastal fringe, reflecting how broadly demand has spread across the city's outer and middle rings. Wanneroo suburbs such as Alkimos and Yanchep have benefited from ongoing residential development, while Belmont - Victoria Park, anchored by suburbs such as Victoria Park and East Victoria Park, stands out as the only top-10 region with strong inner-ring proximity to the CBD.

Thinking of selling or investing in Perth? Compare local agents or get a free property report with OpenAgent.

View agent & property tools

Our powerful property tools